Why Saylor Actually Sold Bitcoin

The 8-K everyone is staring at this morning is about regulatory mechanics, not market timing. And the last time he sold, bitcoin went on to run more than seven times higher.

Strategy filed an 8-K yesterday morning disclosing that the company sold 32 bitcoin between May 26 and May 31 for approximately $2.5 million, at an average price of $77,135 per coin. It was the first net bitcoin sale by the company in four years, since a December 2022 tax-loss harvesting maneuver. The proceeds are earmarked for the company’s STRC perpetual preferred dividend. MSTR was down roughly 5% on the day. Bitcoin slipped to a fresh two-month low under $72,000 in the hours after the filing hit the tape. The crypto press is doing what the crypto press does, which is yelling about whether this is the top, whether Saylor has finally capitulated, whether the bitcoin maximalist thesis is broken, and whether the four-year “never sell” promise was always a lie.

They are asking the wrong question.

The right question is why Saylor sold, and the honest answer is one that almost nobody in this industry is set up to give you, because the honest answer requires having been in a specific room three weeks ago that almost nobody else was in.

I was in that room.

Three weeks ago, after Saylor said on Strategy’s Q1 earnings call that he would “probably sell some bitcoin to pay a dividend just to inoculate the market and send the message that we did it,” he came on the Wolf Of All Streets podcast for the first major interview where he had to defend that statement publicly. The booking came with a condition that the show has never been asked for in its entire run. Strategy’s team told us in advance that they would need the full transcript and raw video of our conversation as soon as possible after recording. They told us this was a new procedural requirement Strategy had recently put in place. Any speaking engagement by a company executive that touched on the pending shareholder vote to convert STRC’s dividend payment schedule from monthly to semi-monthly would have to be filed with the SEC, same day, by 5:30 pm Eastern. Any conversation with Saylor about bitcoin and dividends would inevitably touch on the amendment. So the interview was going to be filed.

I’ll say that one more time, because the implication takes a second to land. Strategy told us in advance, as a condition of doing the interview, that every word Saylor said on my podcast was going to be on the SEC’s desk before the end of the day.

That is not how casual podcast appearances work. That is how regulated communications work. The Saylor who walked into that interview was not a CEO chatting with a friendly host. He was an executive making a disclosure-level statement in front of his own legal and corporate-affairs team, with the full knowledge that the record of the conversation would be filed in connection with a pending corporate action. The statements he made on that show carry roughly the same weight as an earnings call, an 8-K, or a proxy statement. They are part of the official record.

Now read yesterday’s 8-K with that context.

Strategy has $15.5 billion in preferred stock notional outstanding across four series, paying roughly $1.5 billion in annual cash dividend obligations. The biggest piece of that stack is STRC, the Stretch perpetual preferred, currently paying 11.50%. Strategy is in the middle of trying to extend the STRC dividend payment schedule from monthly to semi-monthly, a shareholder vote that requires SEC review of every material communication by company executives. The company is also in the middle of expanding its at-the-market issuance programs to include up to an additional $21 billion of MSTR common, $21 billion of STRC, and $2.1 billion of STRK. Every one of those filings goes across an SEC desk that is now openly tracking what Saylor says in public about how the dividends get funded.

Without an actual, disclosed, on-the-record bitcoin-to-cash-to-dividend round trip, the entire premise that the preferred stack is backed by bitcoin is closer to marketing language than securities-law-compliant disclosure. Yesterday’s 8-K creates that precedent. The 32 BTC sale is not the company’s first step into selling. It is the company’s first step into proving, in the regulatory record, that bitcoin actually functions as a collateral asset behind the dividends rather than just being mentioned in the marketing material around them.

The size of the sale tells you everything about its purpose. Thirty-two bitcoin is $2.5 million. Strategy’s monthly STRC dividend run rate is roughly $100 million. The bitcoin sale paid for less than a single day of the company’s preferred dividend obligations. The actual dividend funding for the period came from the $128.3 million in MSTR common stock that the company issued through its ATM during the same window. The 32 BTC was the headline. The $128.3 million in equity was the substance. The bitcoin sale was a compliance act dressed up in a press release.

The crypto press, predictably, focused on the 32 and missed the 128.3.

Arch Public continues to innovate. Over the next two months we will be launching equities algorithmic tools as well as our proprietary Arch AI. As always, our Concierge Program members will get access first – and at discounted prices. Our current Concierge Program prices have never been lower than they are today. Join us and experience the difference.

Now for the historical context, because this is the part the panic crowd is going to hate.

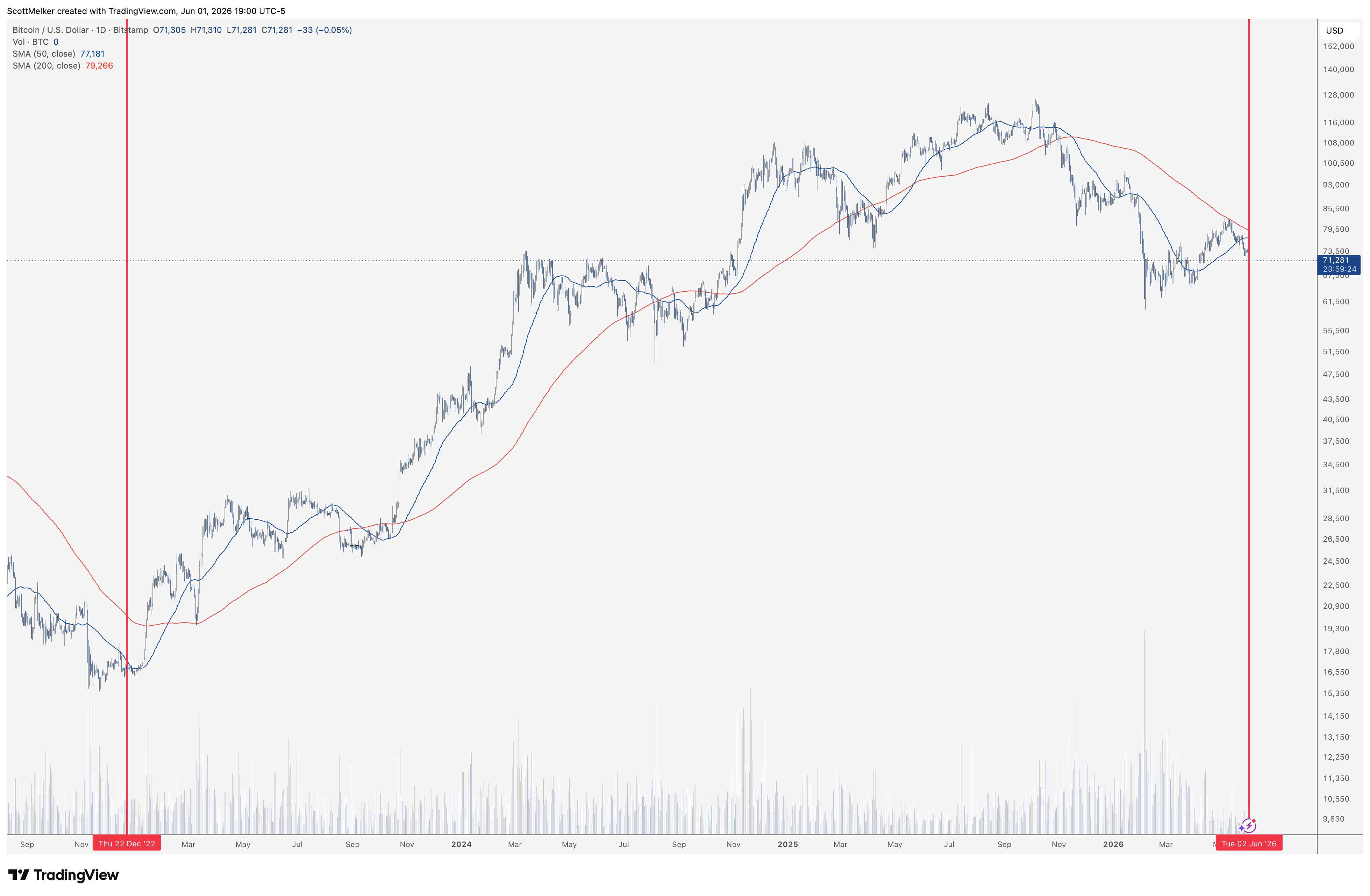

The last time Strategy sold bitcoin was December 22, 2022. The company sold 704 BTC at an average price of $16,776 per coin, for $11.8 million in proceeds. Bitcoin had bottomed about five weeks earlier, in mid-November 2022, at around $15,500. So the last time Saylor sold, bitcoin was within roughly 8% of the deepest low of the 2022 bear market.

Two days later, Strategy bought back 810 bitcoin at an average of $16,800 per coin. The four-day window in December 2022 was net accumulation, not net selling. Saylor sold a small amount to harvest a tax loss against prior capital gains and immediately reaccumulated more bitcoin than he had sold. The headlines at the time said Saylor was dumping. The reality was that he ended the week with more bitcoin than he started.

Anyone who panicked and sold their bitcoin alongside him in December 2022 missed one of the biggest accumulation cycles in the history of the asset. I am not saying this cycle repeats. I am saying the last time the largest corporate bitcoin holder on Earth sold a small amount of bitcoin to satisfy a specific corporate need, the smart money was not selling alongside him. The smart money was buying. The chart above speaks for itself. What you do with it is your call.

Now let me give you the honest bear case, because the bull case is only worth taking seriously if the bear case is named accurately.

The genuine question underneath yesterday’s filing is not whether Strategy can survive its preferred obligations. It can, easily, and the math is not particularly close. Bitcoin needs to appreciate at just 2.3% annually for Strategy’s existing holdings to cover the STRC dividend obligations in perpetuity without selling common stock or any additional bitcoin. That is the number Saylor disclosed on the Q1 call. At 2.3% a year, the company’s existing 843,706 bitcoin throws off enough appreciation to fund the preferreds forever. Bitcoin has averaged well above that threshold over any multi-year period in its history.

The real question is what happens to the equity flywheel that drove MSTR’s outperformance over the past five years. That flywheel depended on MSTR trading at a premium to the underlying value of its bitcoin holdings, which let Strategy issue equity above NAV and use the proceeds to buy more bitcoin, gradually growing bitcoin-per-share. That premium peaked above 2.6x in late 2024. It compressed to 1.91x by July 2025, then to 1.23x by March, and as of the latest data MSTR’s mNAV is sitting at 0.94x. The stock is trading below the value of the bitcoin on its balance sheet, the first sustained sub-NAV print since January 2024.

When MSTR traded at 2x NAV, every dollar of equity Strategy issued created accretion on a bitcoin-per-share basis. At 0.94x, equity issuance at the current price is technically dilutive on the same basis. Strategy issued $128.3 million in MSTR common stock during the May 26 to May 31 window anyway, because the preferred dividend obligations are continuous and the company has multiple capital allocation priorities running in parallel. They also spent $1.38 billion that same week to retire $1.5 billion in face value of their 2029 convertible notes at an 8% discount to par, which is exactly the kind of opportunistic move a well-managed balance sheet makes when it has the cash to do it. The USD Reserve sits at $900 million, down from $2.2 billion at the start of the year, with the bulk of that drawdown explained by the convertible buyback.

That is what an active capital allocation playbook looks like. It is not what distress looks like. Strategy has $10.3 billion in preferred obligations and $8.25 billion in remaining convertible debt, which is a large stack but not an unsustainable one against an underlying treasury that is still one of the strongest in corporate history. The 32 BTC sale was small enough to be a rounding error on a position of 843,706 coins. The company has $26.1 billion of remaining ATM capacity. The textbook accretion engine is running less efficiently than it was a year ago, but Strategy has other levers and they are using them deliberately.

The genuine bear case is not that Strategy fails. It is that the premium does not recover, the equity flywheel stays muted for an extended period, MSTR trades sideways to down even while bitcoin grinds higher, and the 5x leverage that made the stock outperform on the way up disappears in a slow grind sideways. That is a real risk for MSTR shareholders. It is not a risk for Strategy as a corporate entity, and it is not a risk for bitcoin holders watching from the outside.

The honest read of yesterday’s filing is that Saylor did exactly what he said he was going to do on the Q1 call, at the size he said he would do it, with the regulatory context he had set up in advance. A CEO under pressure does not get to be that selective. A CEO running a sophisticated, multi-instrument capital allocation playbook does. The 32 BTC sale was the smallest amount of bitcoin he could plausibly call a sale. It generated the SEC disclosure precedent he needed for the STRC amendment and the next $44 billion in ATM issuance. It established the legal foundation that bitcoin functions as collateral rather than just being mentioned in marketing material. And it cost the company less than 0.004% of its holdings to do it.

That is not pressure. That is precision.

The crypto press is going to spend today arguing about whether Saylor lost the plot. The real story is that he did not.

Watch the filings. Not the personalities.

And if you happen to feel a twinge of fear opening your portfolio this morning, do me a favor and pull up the chart above one more time. Just look at it for a minute.

Then make your own decision.

Cardano Killed Its Own Summit By One Point.

Cardano Foundation cancels 2026 summit after treasury funding vote falls just short

The Foundation’s 7.8M ADA ($2M) summit funding proposal hit 65%, one point short of the two-thirds threshold. Both Hoskinson and CEO Gregaard publicly endorsed it. The community voted them down anyway. On-chain governance bites the people who built it.

Sui Halted Three Times. Foundation Admits Risky Fix.

Sui Admits it Deployed a Known-Risk Fix That Triggered Another Network Halt

Sui mainnet froze three times across May 28-29 from a v1.72 gas-charging bug. The Sunday post-mortem admits the team “knowingly deployed” a risky interim fix that then triggered. SUI down 19% on the week. Move-language was supposed to be the answer to Solana’s reliability problems.

Japan Wants Crypto ETFs And A Yen Stablecoin Empire.

Japan’s ruling party supports crypto ETF trading, yen-based stablecoins

The LDP handed the Finance Minister a proposal Sunday calling for crypto ETF legalization and yen stablecoin promotion across Asia. The world’s third-largest economy just declared it wants its currency on chain across the entire region. The dollar’s head start is about to get tested.

Crypto Funds Bled $1.67 Billion. Worst BTC Week Of 2026.

Bitcoin ETPs face worst 2026 outflow as $1.67B leaves crypto funds

CoinShares clocked $1.67B in outflows last week, with Bitcoin alone shedding $1.44B, the worst BTC weekly outflow of 2026. Three negative weeks have drained $4.21B. AUM is at $141B, lowest since April. The January-February pattern delivered five straight negative weeks. Watch the streak.

Bitcoin CRASHES Below $72K As Saylor Sells For The First Time

My Platforms And Sponsors

Arch Public - It’s a hedge fund in your pocket. Built for retail traders, designed to outperform Wall Street. Try emotionless algorithmic trading at Arch Public today.

Promote your brand with The Wolf of All Streets. For sponsorship and partnership opportunities, contact info@thewolfofallstreets.io.

The Wolf Pack - My Telegram group where I share daily market updates, real-time observations, and ongoing discussions with the community. There’s a dedicated channel and group chat, and it’s completely free to join.

The Crypto Advisor - My weekly newsletter for registered investment advisors, combining macro trends, Wall Street insights, and crypto – all in one place..

X - I spend most of my time on X, contributing to CryptoTownHall every weekday morning, sharing random charts, and responding to as many of you as I can.

YouTube - Home of the Wolf Of All Streets Podcast and daily livestreams. Market updates, charts, and analysis!

The views and opinions expressed here are solely my own and should in no way be interpreted as financial advice. Every investment and trading move involves risk. You should conduct your own research when making a decision. I am not a financial advisor. Nothing contained in this e-mail constitutes or shall be construed as an offering of financial instruments or as investment advice or recommendations of an investment strategy or whether or not to "Buy," "Sell," or "Hold" an investment.

Thanks for reading The Wolf Den! Subscribe for free to receive new posts and support my work.

you clowns dont realize that shitcoin is in a bear market

you are long in a bear market ??

you must either be short or out

or you are going to lose ALL your money

i have told you for months SHITCOIN IS A ZERO

go back and check your comments back to 120 k

SBIT ............OHHHHHHHHHHHHHHH MAMMA !!!!!!!