The Wolf Den #671 - Is Financial Literacy On The Rise?

I took a guess. I was wrong.

Welcome to The Wolf Den! This is where I share the news, my ideas about the market, technical analysis, education and my random musings. The newsletter is released every weekday and is completely FREE. Subscribe!

THIS NEWSLETTER IS SPONSORED BY MEXC!

Sign up using my link to MEXC and receive:

* Up to a $9,100 sign up bonus 🔥

* Available for US users 🔥

* 10% cashback on ALL trading fees 🔥

* 0 fees on ALL spot/futures maker orders 🔥

In This Issue:

Is Financial Literacy On The Rise?

Legacy Markets

ARK Has Big Ideas For Bitcoin And Crypto

Not All Crypto Competition Is Healthy

Why The Largest Banks Want Your FTX Claims | Matt Sedigh Explains How Bankruptcy Market Works

Is Financial Literacy On The Rise?

“Is financial literacy on the rise?” My gut response to this question would be yes, given the amount of available free information, the access to this information and a presumed general increase in interest in financial markets..

I may be wrong.

A few caveats: (a) this is an extremely complex and multi-faceted question (b) I am not a financial historian or expert in sociology (c) this is based solely the United States and (d) financial literacy means more than just understanding the market.

According to Investopedia, “financial literacy is the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing. The meaning of financial literacy is the foundation of your relationship with money, and it is a lifelong journey of learning.”

Prior to sharing what the experts are saying, I want to justify my “hunch.” New forms of financial content are on the rise including podcasts, newsletters, blogs, and e-books. There is a mountain of evidence to support this observation. But is this enough to increase financial literacy?

I started my research in the same manner that you would - I googled, “is financial literacy on the rise,” and “financial literacy in the U.S.” I was disappointed with the results.

Financial literacy is decreasing.

There are various methods to assess this question, but one way to gauge the severity of the situation is to examine the emergency savings and debt levels of Americans. Although these observations may not reveal the full picture, let's briefly examine them.

Americans Aren’t Prepared

“Recent data from Prudential reveals that many Americans aren't prepared. In a survey of younger and older Americans alike, 50% of all respondents said they have less than $500 in the bank, or no emergency savings fund at all.” - SEE HERE

Americans Have A LOT Of Debt

“The percentage of Americans in debt depends on what type of debt is being reported. According to the Urban Institute, more than 64 million Americans carry credit card debt. The Experian study also found that 340 million Americans are currently carrying some form of debt.” - SEE HERE

Of course, some Americans use debt to their advantage and have convertible assets for emergencies, but this is an exception rather than the norm. There is also a distinction between good debt and bad debt. Mortgages on primary residences are generally considered "good debt" as they are repaid steadily over time while equity is accumulated. Bad debt, on the other hand, often takes the form of unpaid credit card balances, and the average American has more bad debt than good.

To further illustrate this point, let's look at what some broad surveys have found.

Only Half Of The U.S. Population Is Financially Literate

“Financial illiteracy is an increasingly large problem in the United States, a fact especially true for minority groups in lower socioeconomic classes. According to a recent survey conducted by Standard & Poor’s, only 57% of U.S. adults are financially literate.”

On More Complex Issues, It Gets Worse

“Today, only about one-third of Americans have a working understanding of interest rates, mortgage rates, and financial risk, according to the Financial Industry Regulatory Authority. And this measure of financial literacy has fallen 19 percent over the past decade.” - TIME

More Reputable Sources Confirm What We Have Learned

“Our findings indicate steady declines in people’s financial literacy, with comparable increases in their likelihood of reporting they did not know the correct answer. We observed the largest declines in correct responses for questions about inflation and risk diversification, while the largest increases in “don’t know” responses were in those pertaining to interest rates and mortgages.” - Finra Investor Education Foundation

So why does this paradox exist? Despite the growing number of retail investors and the emergence of new educational platforms, it seems that financial literacy among Americans is decreasing. The answer may lie in the fact that these developments do not necessarily translate to greater financial literacy for the general public. The surge in curiosity about the Fed and crypto has attracted a new segment of investors, but this does not mean that Americans as a whole are effectively saving and investing.

We are a small echo chamber.

We must strive to do better, starting with educating our youth and making financial literacy accessible to everyone. Investing in knowledge pays dividends that last a lifetime, and it is never too late to learn. A world with greater financial literacy means that the Fed cannot easily erode our savings and Bitcoin is considered a credible alternative. Financial literacy equips individuals to take care of their financial well-being, so they can enjoy life's pleasures without worrying.

*I APOLOGIZE FOR THE LACK OF A NEWSLETTER YESTERDAY AND FOR THE TIMING OF TODAY’S NEWSLETTER. I AM TRAVELING ACROSS TIME ZONES AND HAVE HAD VERY LIMITED ACCESS TO INTERNET. I WILL BE BACK TO REGULARLY SCHEDULED PROGRAMMING TOMORROW.

Legacy Markets

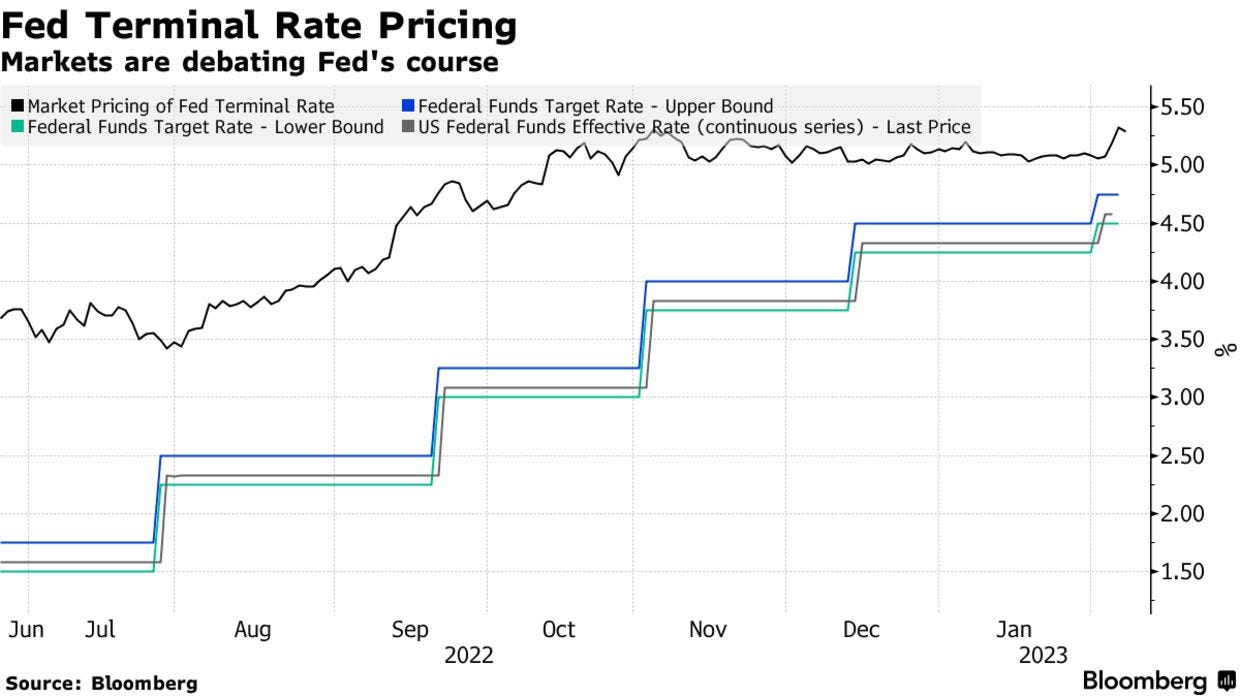

Stocks in Asia, along with US and European equity futures, are rising ahead of comments from Federal Reserve Chair Jerome Powell. A gauge of the region's shares increased by 0.8%, reducing losses from the largest two-day drop in four months, as investors ponder the chances of the Fed maintaining its monetary policy. Hong Kong's tech stocks experienced some of the strongest gains, while US equities saw a decline due to rising bond yields. Baidu Inc. rose 15% after announcing plans to launch a ChatGPT-like bot in March. Meanwhile, Australia's currency rose and bonds fell after the central bank increased its key rate to the highest in 10 years, and investors are considering Powell's comments on rate cuts later in 2023. The yen gained after Japan reported a surprising jump in nominal wages in December, while the Citigroup sees dollar strength as a risk to stock markets. In India, most of Adani Group's stocks climbed after the family's move to prepay $1.11 billion of borrowings alleviated investor fears. The cautiousness in global markets is being reinforced by geopolitical concerns, such as the US imposing a 200% tariff on Russian-made aluminum. Oil rose for a second session after Saudi Arabia increased its crude prices to Asia, and gold steadied.

Key events:

US trade, Tuesday

Fed Chair Jerome Powell interviewed by David Rubinstein at the Economic Club of Washington, Tuesday

President Joe Biden delivers the State of the Union address before Congress, Tuesday

US wholesale inventories, Wednesday

New York Fed President John Williams is interviewed at Wall Street Journal live event, Wednesday

US initial jobless claims, Thursday

ECB President Christine Lagarde participates in EU leaders summit, Thursday

Bank of England Governor Andrew Bailey appears before Treasury Committee, Thursday

US University of Michigan consumer sentiment, Friday

Fed’s Christopher Waller and Patrick Harker speak, Friday

Some of the main moves in markets:

Stocks

S&P 500 futures were little changed as of 1:57 p.m. Tokyo time. The S&P 500 fell 0.6%

Nasdaq 100 futures rose 0.1%. The Nasdaq 100 fell 0.9%

Japan’s Topix rose 0.2%

Australia’s S&P/ASX 200 fell 0.5%

Hong Kong’s Hang Seng rose 0.8%

The Shanghai Composite rose 0.3%

Euro Stoxx 50 futures rose 0.1%

Currencies

The Bloomberg Dollar Spot Index fell 0.1%

The euro was little changed at $1.0733

The Japanese yen rose 0.3% to 132.28 per dollar

The offshore yuan rose 0.2% to 6.7944 per dollar

The Australian dollar rose 0.7% to $0.6931

Cryptocurrencies

Bitcoin fell 0.1% to $22,882.45

Ether fell 0.4% to $1,631.93

Bonds

The yield on 10-year Treasuries declined two basis points to 3.62%

Japan’s 10-year yield was little changed at 0.49%

Australia’s 10-year yield advanced 15 basis points to 3.61%

Commodities

West Texas Intermediate crude rose 1% to $74.87 a barrel

Spot gold rose 0.3% to $1,873.35 an ounce

ARK Has Big Ideas For Bitcoin And Crypto

I have two images to share in this section that speak for themselves. Cathie Wood, the queen of high-end investment research, supports her well-known bullish crypto predictions through these images. While a 25x growth for the crypto market may seem far-fetched, it is actually within reach when considering the expansion of the money supply, which is likely to drive exponential growth across all markets in the coming decade.

The second image was popular on crypto Twitter and was the most talked-about page from the report. This year's research, which includes a bear case, base case, and bull case, is unique in that it offers a comprehensive outlook. The $1.48 million target may seem ambitious, but when you consider the required penetration rate into the total addressable market, it becomes more plausible.

Assuming Bitcoin takes up significant positions in the gold market and the remittance market, the penetration rates are all under 10%. Bitcoin has the potential to outperform gold and reach a price between the base case at $682,000 and the bull case at $1.48 million by 2030. With financial literacy on the rise and easy access to education, this future is becoming more achievable every day.

Not All Crypto Competition Is Healthy

Typically, competition is considered healthy for the industry. But in some cases, it can be detrimental. Goliath VC a16z has put its entire Uniswap position up for a vote against a proposal that would benefit the crypto industry, but happens to also be a competitor.

The background is that a16z is a major investor in LayerZero, a crypto bridge, while Jump Capital (a VC competitor) invests in Wormhole, another bridge. The proposal is to deploy Uniswap V3 on BNB Chain, using the Wormhole bridge, which would be beneficial to the industry, except for a16z, which seeks to outperform its competition.

The voting ends on February 10th, and historically, Uniswap DAO members tend to wait until the last minute to vote, so there is hope that the proposal will not pass. Although the decision itself may be minor in the world of crypto, its implications are far-reaching. If decentralization is the goal, venture capitalists should not hold all the voting power.

ChrisBlec summarized it well - “anti-competition cartels in DeFi are REAL.”

Why The Largest Banks Want Your FTX Claims | Matt Sedigh Explains How Bankruptcy Market Works

XClaim is a marketplace that connects bankruptcy claim holders with potential buyers. They recently made the news when it was announced that FTX claims were trading at 13 cents on the dollar. In this episode, Matt Sedigh, founder of XClaim, explains how this market works, why claims will be tokenized, and who the biggest buyers of bankrupt crypto companies’ claims are.

In this episode with Matt, we discussed:

What is Xclaim

Crypto bankruptcies

Business model

FTX case

Voyager

How people find out about Xclaim

Trading claims

How price of Bitcoin influences the price of the claims

Tokenizing claims

Distressed assets players

Crypto native funds trading claims

$35 billion of funds locked

Genesis claims

Lack of regulation

Fraud is still legal

Price discovery

Use cases for claims

Bankruptcy claims & tokenization

Is contagion over?

Claims business is huge

The views and opinions expressed here are solely my own and should in no way be interpreted as financial advice. Every investment and trading move involves risk. You should conduct your own research when making a decision. I am not a financial advisor. Nothing contained in this e-mail constitutes or shall be construed as an offering of financial instruments or as investment advice or recommendations of an investment strategy or whether or not to "Buy," "Sell," or "Hold" an investment.