The Wolf Den #1218 - Crypto Credit Cards Are The Craze

Are you using one?

Welcome to The Wolf Den! This is where I share the news, my ideas about the market, technical analysis, education and my random musings. The newsletter is released every weekday and is completely FREE. Subscribe!

Today’s Newsletter Is Made Possible By Arch Public!

Arch Public enjoyed our time at The Bitcoin Conference in Vegas!! We enjoyed meeting many of you and hosting industry titans in our Arch Public Lounge with Scott.

As Bitcoin remains above $100K the constant chatter was finding ways to generate yield. As you can imagine, our products are uniquely qualified to do just that!

The Bitcoin Yield Algorithm produces 20% APY and 25% CAGR. Extraordinary numbers. Keep your Bitcoin (and accumulate more) while harvesting volatility and turning into yield.

In This Issue:

Crypto Credit Cards Are The Craze

Bitcoin Thoughts And Analysis

Markets Stabilize As Investors Bet On Contained Israel–Iran Conflict

What Happened To Sharplink Gaming?

The Solana ETFs Are Inching Towards The Finish Line

Bitcoin Backed Mortgages Are Here

GameStop Sizes Up Its Debt Offering

Bitcoin Will Replace The Dollar | Jack Mallers Explains Why

Crypto Credit Cards Are The Craze

Last week, Coinbase announced its upcoming credit card, which prompted me to do a quick write-up on the details. I think these products are genuinely interesting - just to be clear, I get zero benefit from saying that. So today, I wanted to share a few more thoughts and take a look at some of the most popular crypto cards out there. I know this is a bit different from my usual coverage, but I think it offers a lot of practical value for a lot of you.

There’s a nagging voice in the back of my head reminding me what happened last cycle - Voyager, Celsius, BlockFi - all offering high yields for holding assets, only to collapse with customer funds. Part of me wants to lump crypto credit cards into that same bucket. But I also think the companies offering these cards today are approaching things more cautiously and, knock on wood, have learned from what didn’t work last time.

The difference now is that crypto credit cards aren’t promising free yield or unsustainable returns just for parking your assets with them. In the last cycle, platforms like Voyager, Celsius, and BlockFi dangled high APYs to attract deposits - returns that were often fueled by risky lending practices or outright mismanagement. Today’s crypto credit cards are structured more like traditional rewards programs: you spend, and you earn a percentage back in crypto. It’s a more sustainable model, tied to actual usage rather than speculative lending. While they’re still not without risk, they don’t carry the same illusion of ‘free money’ that defined so many of the failed products from the last cycle.

Also, I’m only going to share details on three options today - all of which I believe are among the safest available. That said, it’s important to remember: if you choose to sign up for one of these products, you assume all the risk. Do your own research, understand the terms, and make sure the product aligns with your comfort level and financial goals. Nothing in this space is risk free. So, on that note, let’s start with Robinhood’s Gold Card.

Visually speaking, this card is stunning. I know for some of you that matters - and honestly, the picture doesn’t do it justice.

Robinhood also earns bonus points for kicking off this new craze. Crypto credit cards have technically been around for over a decade, but Robinhood was the first mainstream company to launch this new generation of cards - crypto‑reward credit cards, with added perks and the backing of traditional banking partners.

Here are some key details:

The card weighs 17 grams; it’s pure stainless steel.

It’s a Visa card.

It’s exclusively for Robinhood Gold members.

No annual fee.

You receive 3% cashback.

5% cash back when you book travel through the Robinhood Travel portal.

Remember, this isn’t DeFi - every credit card is going to require your personal information. These are crypto products, but they’re not exactly in line with the ethos of crypto.

You may have also heard about the solid gold credit card. It’s not easy to earn, but if you manage to refer 10 people to Robinhood Gold, you’ll be upgraded to a literal solid gold card. It weighs 36 grams and is made of 10K gold.

The value of this thing is insane.

The catch behind the Robinhood Gold Card is that you have to be a member of Robinhood Gold. The good news is that it’s affordable. It’s $5 per month or $50 per year with a ton of other benefits. Here are a few:

There’s a good chance some of you Robinhood users already have Robinhood Gold and in that case, the credit card is available to you with no additional fee. Personally, I think this card is a far better choice than your average run-of-the-mill bank credit card, unless you’re a high-net-worth individual with access to exclusive premium cards. Crypto credit cards aren’t going to give you the luxury travel perks or concierge services that top-tier premium cards offer, but they do provide unique benefits.

On that note, let’s look at Coinbase’s One Card coming out this fall.

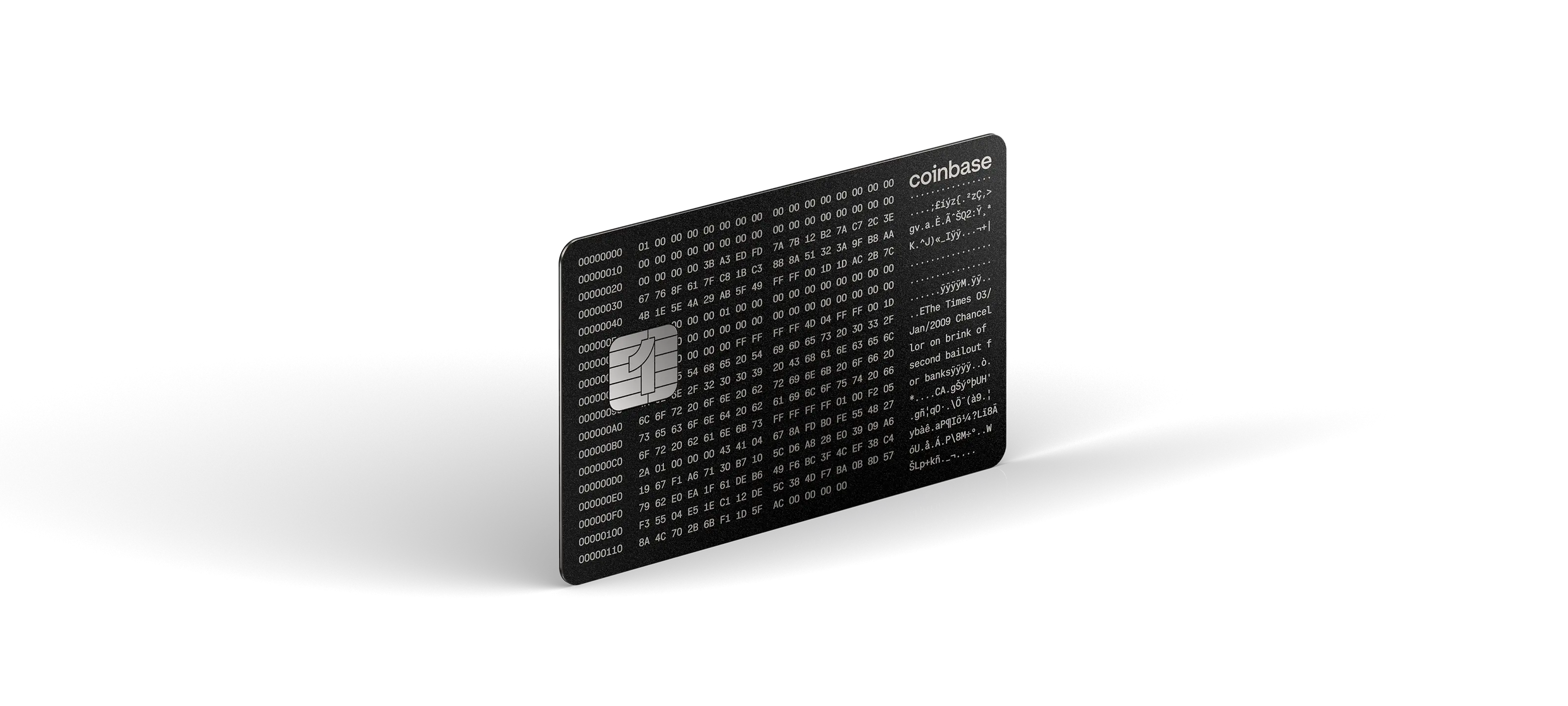

Last week Coinbase announced it is releasing its own credit card this coming fall. It works differently than Robinhood’s and comes with different perks all together.

Visually, the card is very different from the Robinhood’s but still very unique in its own right.

It’s hard to read from the image, but the graphic is the genesis block and includes the Easter egg, “Chancellor on brink of second bailout for banks,” referencing the headline from the UK’s The Times newspaper on January 3, 2009 - the very day Bitcoin’s first block was mined, highlighting the financial crisis that inspired its creation. Coinbase’s design team needs a raise.

Here are some key details:

The card weighs 17 grams; it’s pure stainless steel.

It’s an American Express card.

It’s exclusively for Coinbase One members.

No annual fee.

You receive up to 4% cashback.

What makes this card different is that “The more assets you hold on Coinbase, the more bitcoin you earn on your purchases.” Not as much information is available about the card at this time, but this is key, “Cardholders can earn up to 4% bitcoin back on their purchases. The more assets you hold on Coinbase the higher your rewards rate. You can hold any asset including USDC or USD to qualify. We’ll share more when the card goes live.” If Coinbase announces an insanely high requirement to qualify for the 4% rewards, that would be disappointing. A lot of the card’s value really depends on how accessible that top-tier rate is and what the required asset levels on the platform look like.

Fortunately, I know a lot of people already hold assets on the platform, so this could be a no-brainer for those who do. The catch on this card is you have to be a Coinbase One Member to access the card, which isn’t exactly cheap:

The good news is that with the card’s release, Coinbase One will soon offer annual memberships starting at just $49.99 per year, making it a bit more accessible to all customers. What this means is that if a customer qualifies for 4% back in Bitcoin for the entire year, you’d need to spend $1,250 annually to break even on the membership cost - anything above that, and you’re in the green. Furthermore, this doesn’t include the perks of being a Coinbase One member:

If you are already trading on Coinbase, have USDC earning yield, assets staking, and an interest in Base, this membership is a no-brainer. The big question surrounding this card is: how much in assets will you need to earn 4% cashback? The answer could make or break its appeal.

Last but not least, I want to examine the Gemini Credit Card.

This card isn’t just available in Bitcoin, orange, you can also order it in black, silver and rose colors.

Two key features make this card stand out: first, cashback rewards vary based on the category of your purchase; second, you can easily choose which crypto you want to earn - selecting from over 50 options. That’s something neither of the two cards above emphasized. While Robinhood technically lets you use your points to buy any asset, Gemini leans into this flexibility and appears to make the process smoother - if not more cost-effective as well.

For someone who spends heavily in the blue and red reward categories, this card is very appealing. If not, it doesn’t stack up quite as well compared to the other options.

Here are some key details:

The card is plastic (I believe).

It’s Mastercard

It’s available to everyone.

No annual fee or membership required.

You receive anywhere from 1% to 4% cashback on purchases.

Other major selling points of this card include a $200 Bitcoin reward when you spend $3,000 within the first 90 days, and the fact that it comes with no costs - no subscription fees or annual costs like the two cards mentioned above. That trade-off helps explain why the cashback benefits aren’t quite as strong.

That wraps up the details on these three cards. I'm sure there are other decent options out there, but I’d caution against signing up for a card that isn’t affiliated with a major, reputable platform. Keep in mind, all of these cards reserve the right to change their rewards at any time - and I wouldn’t be surprised if they do, especially if a bear market hits and it becomes harder to justify high cashback rates or boosted rewards on stablecoins and staked assets.

What actually makes me feel a bit more confident about these cards is that most of them come with a fee (with the exception of Gemini). That might sound counterintuitive, but it’s a good reminder that the better rewards aren’t truly ‘free’ - they come at a cost, which, in a way, feels safer and more sustainable. When companies charge a subscription or annual fee, it suggests they’re not relying solely on risky lending practices or unsustainable incentives to fund high cashback rates. Instead, there's a more balanced model in place, which gives me more confidence that these rewards could actually last.

My main takeaway on these cards is that if you’re already familiar with - and enjoy using - these platforms, the credit card feels like a natural extension of your experience. If you’re someone who already has three or more cards, it might be a good time to consider consolidating and streamlining your finances by shifting part of it into crypto. These cards offer a way to stay engaged with the space while earning rewards in assets you believe in, making them especially appealing for users who are already invested - literally and figuratively - in crypto.

That sums up all my thoughts on crypto credit cards. None of these companies asked me to share this, and I wasn’t paid a penny. I know the intro might read like an advertisement, but it’s not. I genuinely want to help you all make informed choices, I like these companies, and I believe these cards could be a great fit for the right person.

Bitcoin Thoughts And Analysis

Bitcoin is once again pressing against the midpoint of its recent trading range after bouncing off the 50-day moving average near $105,000. Today’s candle shows solid follow-through from that bounce, reclaiming short-term structure and closing back above the key $105,787 level.

The broader structure remains a consolidation between $100,700 support and $112,000 resistance – with Bitcoin repeatedly testing both boundaries without breaking out. The most recent rejection at $112K marked the second failed attempt to clear that level, suggesting the presence of strong supply overhead. However, the continued defense of $105K and especially the higher low at $100,700 keeps the bullish structure intact for now.

The 50-day moving average has now been tagged multiple times and held as dynamic support, reinforcing its relevance in this trend. Meanwhile, the 200-day MA remains well below at $95K, and continues to slope upward, confirming broader trend health.

Volume remains relatively light during this bounce, which could be a cautionary signal for bulls hoping to see a breakout attempt. A move above $108K–$110K would likely re-ignite momentum toward the $112K top of range, while a clean break above $112K would open the door to a measured move toward $120K.

To the downside, the $100,700–$101,000 area is the line in the sand. A break below that level would invalidate the current higher low structure and put the $92,800 and $88,800 zones back in play as support.

In short, Bitcoin is still range-bound, but technically healthy. The bulls are defending key support levels and the 50 MA, while bears remain active at resistance. The next directional break – above $112K or below $100K – will likely dictate the next major move.

Markets Stabilize As Investors Bet On Contained Israel–Iran Conflict

Markets showed signs of steadying on Monday after Friday’s sharp selloff, as investors reassessed the risks of broader conflict between Israel and Iran. With traders increasingly betting that the hostilities will remain geographically contained, U.S. equity futures rebounded. S&P 500 futures rose 0.5%, signaling a recovery after the index fell more than 1% late last week. Gains were also seen across European and Asian equities, while Treasuries sold off for a second session in a row on inflation concerns, pushing the 10-year yield up to 4.44%.

The commodities complex reflected this tempered sentiment. Brent crude, which had surged as much as 5.5% over the weekend, pulled back 0.4%. Gold also slipped 0.5% from Friday’s record high, as safe-haven demand softened alongside the improved risk appetite.

The broader market narrative remains focused on dip-buying optimism. The S&P 500 had been rallying back toward record highs before the weekend strikes, and many investors believe the conflict won’t expand significantly. “The situation in the Middle East is not making the market shake,” said fund manager Enguerrand Artaz, who expects momentum to stay strong barring a major escalation. “The mood overall is still very much about buying the dip.”

Geopolitics isn’t the only item on investors’ radar this week. Central bank decisions from the Federal Reserve and the Bank of Japan are expected, alongside a Group of Seven summit that may offer further insight into global economic policy and coordination. All eyes will be on how monetary authorities respond to potential inflation risks—especially if oil prices remain volatile.

Stocks

The Stoxx Europe 600 rose 0.2% as of 9:25 a.m. London time

S&P 500 futures rose 0.5%

Nasdaq 100 futures rose 0.6%

Futures on the Dow Jones Industrial Average rose 0.4%

The MSCI Asia Pacific Index rose 0.7%

The MSCI Emerging Markets Index rose 0.7%

Currencies

The Bloomberg Dollar Spot Index fell 0.1%

The euro rose 0.3% to $1.1578

The Japanese yen fell 0.2% to 144.29 per dollar

The offshore yuan rose 0.1% to 7.1815 per dollar

The British pound was little changed at $1.3583

Cryptocurrencies

Bitcoin rose 2.2% to $107,019.01

Ether rose 4.9% to $2,626.14

Bonds

The yield on 10-year Treasuries advanced five basis points to 4.44%

Germany’s 10-year yield advanced four basis points to 2.57%

Britain’s 10-year yield advanced two basis points to 4.57%

Commodities

Brent crude fell 0.4% to $73.94 a barrel

Spot gold fell 0.5% to $3,414.85 an ounce

What Happened To Sharplink Gaming?

SharpLink Gaming is a newer name in the crypto space, so I’ll give a quick refresh. Sharplink is an online betting platform, that launched an Ethereum-based corporate treasury strategy and announced a $425 million private investment in public equity (PIPE) deal. The raise was led by Ethereum infrastructure firm Consensys and included major crypto investors you probably have heard of including ParaFi, Electric Capital, Pantera, and Galaxy Digital. CEO Rob Phythian and CFO Robert DeLucia also participated.

As part of the deal, Ethereum co-founder and Consensys CEO Joseph Lubin was nominated as chairman of SharpLink’s board of directors. Lubin stated that Consensys looks forward to partnering with SharpLink to develop its Ethereum treasury strategy and support its core business as a strategic advisor.

So why did the stock drop over 75% when other treasury companies have been performing well? Good question.

SharpLink’s stock dropped because it filed what’s called an S-3ASR registration statement, which allows over 100 early PIPE investors to sell nearly 59 million shares. Even though the company just raised $450 million to buy Ethereum, the sudden potential for a massive wave of share sales spooked investors. It created fear of dilution -more shares flooding the market could drive the price down, so people rushed to sell before that happened.

What’s important to note is that this kind of filing is common after a PIPE deal, but the scale and timing caught the market off guard. Even though there’s speculation that SharpLink may soon announce a much larger Ethereum purchase (possibly up to $1 billion), the immediate fear of sell pressure outweighed the long-term excitement.

Furthermore, while stock drops following S-3 or PIPE filings are common due to fears of dilution, rebounds can and do happen - especially if the company delivers on its strategy and regains investor confidence. If SharpLink follows up with strong execution, like confirming a major Ethereum purchase or showing the impact of its treasury strategy, the stock could easily recover. But rebounds aren't guaranteed; if selling pressure continues or the market doubts the company’s next moves, the stock will stay depressed.

The Solana ETFs Are Inching Towards The Finish Line

These seven firms have filed S-1 statements for Solana ETFs, all with staking language included: Fidelity Investments, 21Shares, Franklin Templeton, Grayscale Investments, Bitwise Investments, Canary Capital, and VanEck. Apparently, the SEC is actively engaging with the filers - a positive sign that these products are likely to make it across the finish line ahead of other competing assets. That said, the process may still take some time, according to Jeff Seyffart. “I think there needs to be a back and forth with the SEC and issuers to iron out details, so I doubt it. If anyone remembers the Bitcoin ETF launch, there were *A LOT* of filings over the preceding couple months before launch.” The key for Solana - and for ETH staking - is BlackRock. Without their filings or involvement, inflows are likely to remain muted.

Bitcoin Backed Mortgages Are Here

The Peoples Reserve just dropped their official interest rate announcement on the latest episode of The Charlie Shrem Show. For those who don’t know, Charlie’s an OG in the space, a good friend of mine, and one hell of an interviewer. As for the news - the lowest attainable interest rate for their Bitcoin Powered Mortgage (BPM) product is 3.5% APR!

The reason why I took on The Peoples Reserve as a sponsor is because their product makes sense. This rate is lower than both the current U.S. Prime Interest Rate (7.5%), which serves as the anchor rate for TradFi mortgages, and the “risk free” U.S. Treasury bill rate (~4.5%).

How it works: Embracing Michael Saylor’s Digital Asset Framework, Peoples Reserve created a Digital Token Asset called the Peoples Reserve Network (PRN) Loyalty Token. The starting interest rate on Bitcoin Powered Mortgages is directly tied to the borrower’s PRN loyalty level.

Loyalty Levels and Starting Interest Rates have been announced as:

Basic (10.5% APR), Silver (9.5% APR), Gold (8.5% APR), and Diamond (7.5% APR).

Here’s a quote from CJ the founder, “There should be no confusion, Bitcoin is money. Any crypto that tries to compete with Bitcoin is a scam. The PRN loyalty token is not money. It’s a digital utility token designed to compliment Bitcoin, not to compete with it. PRN was strategically engineered to empower responsible savers of Bitcoin as the true ‘risk-free’ borrower, giving them access to the true “risk-free” interest rate. Holding loyalty tokens in your account comes with real economic value. Don’t speculate, calculate your benefits with PRN.”

Their upcoming Loyalty Token sale will take place on July 4 and they’re calling it “We The People Day,” to claim back financial independence and freedom, powered by Bitcoin. I suggest checking out their site if you have the chance and considering a Bitcoin backed mortgage if it makes sense for you.

GameStop Sizes Up Its Debt Offering

GameStop has increased its convertible note offering from $1.75 billion to $2.25 billion, with notes carrying a 32.5% conversion premium and no interest. While the company currently holds 4,710 Bitcoin, it remains unknown its future crypto purchases. The raised funds may be used for general purposes, investments, or acquisitions. Despite the announcement, GameStop’s stock has fallen 24% over the past week, which should rebound once Bitcoin breaks through all-time highs. I’d like to see GameStop continue to buy Bitcoin before other mainstream players are competing at higher prices.

Bitcoin Will Replace The Dollar | Jack Mallers Explains Why

I sat down with Jack Mallers at Bitcoin Las Vegas for The Wolf Of All Streets to talk about how Bitcoin is reshaping the global financial system. From the fall of the 60/40 portfolio to El Salvador’s bold experiment and the rise of Bitcoin treasury companies, this is a front-row seat to the Bitcoin revolution. Jack doesn’t hold back – this conversation will change how you think about money, power, and the future.

My Recommended Platforms And Tools

Aptos - The blockchain network with everything you need to build your big idea. Unrivaled Speed, Unprecedented Trust, and an Unstoppable Community on Aptos.

Arch Public - It’s a hedge fund in your pocket. Built for retail traders, designed to outperform Wall Street. Try emotionless algorithmic trading at Arch Public today.

Peoples Reserve - Use Bitcoin as pristine collateral with Peoples Reserve - where wealth is built smarter through Bitcoin-powered finance.

Trading Alpha - Trade With Confidence! My new go-to indicator site and trading community. Use code '25OFF' for a 25% discount.

X - I spend most of my time on X, contributing to CryptoTownHall every weekday morning, sharing random charts, and responding to as many of you as I can.

YouTube - Home of the Wolf Of All Streets Podcast and daily livestreams. Market updates, charts, and analysis! Sit down, strap in, and get ready—we’re going deep

The views and opinions expressed here are solely my own and should in no way be interpreted as financial advice. Every investment and trading move involves risk. You should conduct your own research when making a decision. I am not a financial advisor. Nothing contained in this e-mail constitutes or shall be construed as an offering of financial instruments or as investment advice or recommendations of an investment strategy or whether or not to "Buy," "Sell," or "Hold" an investment.

Hey Scott, just a heads up. Venmo also offers a card that pays points in BTC & ETH. Been using one for 2 years. I'm up 187% on my BTC points balance!!