The Wolf Den #1209 - Here’s the Average Net Worth by Age (And Why It Matters)

How do you compare?

Welcome to The Wolf Den! This is where I share the news, my ideas about the market, technical analysis, education and my random musings. The newsletter is released every weekday and is completely FREE. Subscribe!

Today’s Newsletter Is Made Possible By Arch Public!

Arch Public enjoyed our time at The Bitcoin Conference in Vegas!! We enjoyed meeting many of you and hosting industry titans in our Arch Public Lounge with Scott.

As Bitcoin remains above $100K the constant chatter was finding ways to generate yield. As you can imagine, our products are uniquely qualified to do just that!

The Bitcoin Yield Algorithm produces 20% APY and 25% CAGR. Extraordinary numbers. Keep your Bitcoin (and accumulate more) while harvesting volatility and turning into yield.

In This Issue:

Here’s the Average Net Worth by Age (And Why It Matters)

Bitcoin Thoughts And Analysis

US Stock Futures Slip as Trade Uncertainty Remains

Russia’s Largest Bank Launches Bonds Linked To Bitcoin

Circle Is Set To Go Public Later This Week

Consensys Closes Its Deal With SharpLink

Wall Street Panic As Bitcoin Holds Strong - Bottom Confirmed? | Macro Monday

Here’s the Average Net Worth by Age (And Why It Matters)

Everyone has asked themselves this question: am I ahead or behind when it comes to average net worth for my age? While that question can lead to unhelpful comparisons - comparison, after all, is the thief of joy - it can also serve as a useful benchmark to gauge your progress and shape a smarter plan for saving and preparing for retirement.

I'll assume this question is being considered in good faith, so I'll do my best to provide a thoughtful and thorough answer - just be sure to use this information responsibly.

For starters, it makes much more sense to frame the question in terms of the median rather than the average. While most people casually say ‘average’ when talking finances and net worth with friends or family, the problem is that the mean will always be heavily skewed by the wealthiest 1% and not really provide an accurate assessment for our purposes. The median, on the other hand, gives a more complete picture of where the typical person truly stands.

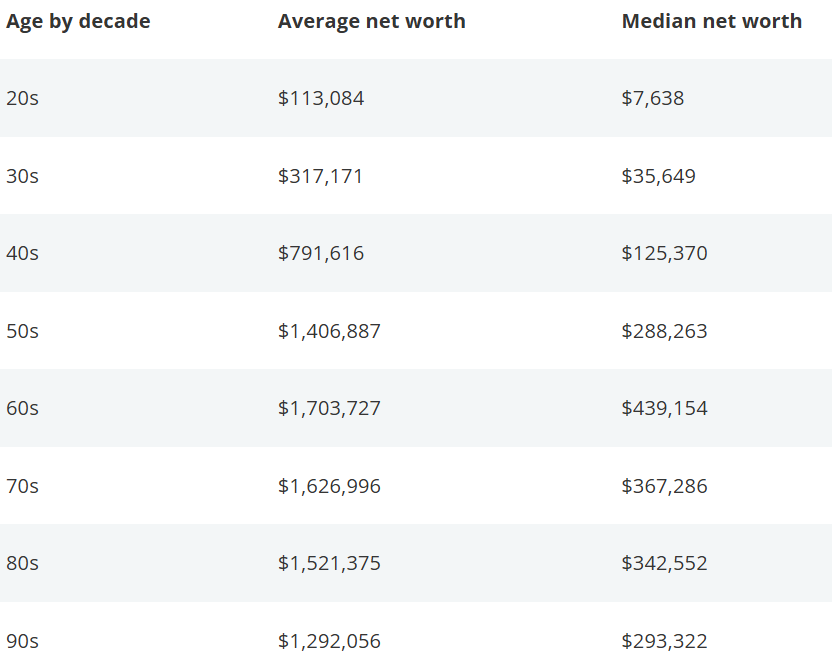

To answer this question, I’m referencing an article from Empower titled “The Average Net Worth by Age in America,” which compiles data from 2019 to 2022. The article was published at the end of last year, so while the numbers aren’t real-time, they’re still relatively fresh, especially considering that net worth data typically lags by a couple of years.

Let’s look at the data:

I know your eyes probably jumped straight to your age and then slid to the right - but there’s more to unpack. Stick with me.

First, I’d like to share some thoughts for each age group. Please note - this is not financial advice. I’m not a professional, and nothing here should ever be taken as such. These are simply my personal views, drawn from a mix of commonly accepted truisms and my own experience.

Also, where you live and what your expenses are greatly matter.

Being single in Phuket, Thailand is a world apart from being married with three kids in New York, New York - and both are completely different from someone who’s retired and restoring vintage sailboats off the coast of Portugal. Life circumstances shape financial needs, goals, and strategies, so there’s no one-size-fits-all approach.

Let’s reshare the numbers, accounting for inflation since the study:

Keep in mind this is a rough estimate - it doesn’t account for rising wages, changes in asset prices, or even the true rate of inflation.

20s: Average ($130,047) Median ($8,784)

30s: Average ($364,446) Median ($40,996)

40s: Average ($910,358) Median ($144,176)

50s: Average ($1,617,920) Median ($331,503)

60s: Average ($1,959,286) Median ($504,027)

70s: Average ($1,870,045) Median ($422,379)

80s: Average ($1,749,581) Median ($393,935)

90s: Average ($1,485,864) Median ($337,320)

Now for my thoughts:

If you are in your 20s, your primary goal should be tackling any debt you've taken on - especially student loans. That might mean living with roommates, skipping on the luxury car, and eating your fair share of PB&Js. Sacrifices now will set you up for massive dividends and freedom later on. Even if you can’t invest how you want to, eliminate the debt!

If you have eliminated your debt, your next focus should be opening up a savings and retirement account (you can technically do this while paying off your debt, you don’t have to go in a specific order). This can be as easy as going to your local bank and asking a banker for help. Even if you can only contribute $50 a month or $10 a week, learning to aside money for your future is the single best habit you can develop. While you're working to eliminate your debt, your other key focus should be asking: how can I advance in my career? How can I increase my earning potential? Laying that foundation early will also pay dividends down the road.

It’s around your 30s when the pressure to ‘keep up with the Joneses’ really sets in. Bill just upgraded to a sleek BMW 5-Series, and the Smiths spent a week at Disney, hitting every park while staying on-site at a four-star hotel. Good for them, but if these things aren't in your budget just yet, don’t rush to take out a loan to force them in. Chances are Bill and the Smiths probably didn’t make the soundest financial decisions when making these purchases and their debts may be on high-interest payment plans.

If you’re going to purchase a house - which I’d argue isn’t essential unless you have a family (personally, I think investing in Bitcoin right now makes more sense) - there’s no need to go overboard. You don’t have to buy your forever home right away. Your newborn won’t know (or care) whether you have an acre of backyard or a small patio. In your 30s, focus on eliminating all debt except your mortgage, and keep that mortgage reasonable - ideally, the home should cost no more than 2.5 times your annual income.

Again, this is common knowledge, I am not claiming to be a financial planner.

If you’re in your 40s, chances are you’ve either already reached your prime earning years or are approaching them soon, depending on your career path. This can be a great time to make progress on outstanding debts, such as your mortgage or business loan - if paying them off early makes financial sense. However, if you have a low-interest rate loan, are financially disciplined, and have a solid savings cushion, there may be little benefit to paying it off ahead of schedule. In situations like these, consulting a financial professional can be a smart move that might save you tens of thousands of dollars or more.

In your 40s, there’s also a good chance you’ll start to see the power of compounding truly take effect. If your net worth falls somewhere between the median of $144,176 and the average of $910,358 - and you have a significant portion invested - you could see annual investment returns ranging from $5,000 to over $100,000, thanks solely to compounding.

This is also the decade when retirement planning becomes critical - if it hasn’t been already. Wear and tear on your body, rising healthcare costs, and expenses related to children can all add up quickly. That’s why it’s essential to have a clear understanding of your annual cost of living, how much you want to allocate toward discretionary spending, and what kind of lifestyle you envision in retirement. The more clarity you have now, the more flexibility and security you can build for the future.

Also, it’s time to enjoy life a little. If that second annual vacation or upgraded BMW has been on your mind for a while - go for it. I invest so I can live well and take care of my family, not to take it all with me to the grave. This is life advice, not financial advice.

By the time your 50s roll around, hopefully you have a very clear understanding of your financial arc for the rest of your life. Your peak earning years are likely behind you, but if your nest egg is substantial, you may be able to live comfortably with less income - or even none at all. Don’t panic if some of your friends have already retired. The average retirement age in the U.S. is still in the low to mid-60s. And chances are, the same friends posting glamorous retirement photos on Facebook are bored 95% of the time.

It’s also key in your 50s to begin restructuring your portfolio. As your income starts to wind down, protecting your net worth should become a higher priority. This might mean shifting away from high-risk assets and seeking greater diversification - such as incorporating bonds (not so compelling anymore), dividend-generating investments, or other income-producing products. The goal is to create a more stable financial foundation that supports your lifestyle while reducing exposure to market volatility as you approach retirement.

For those in your 50s, you're technically approaching the age when you can begin collecting Social Security - but (not financial advice) I wouldn’t rely on it entirely. It’s better to think of it as a bonus, not a guarantee. There’s growing speculation that, due to long-term funding challenges, the U.S. may not be able to fully meet its Social Security obligations in the decades ahead. While it’s unlikely to disappear altogether, future benefits could be reduced unless significant reforms are made.

As for your 60s, I don’t have too much advice - except to say this might be a good time to start thinking seriously about estate planning. That means having a will in place, setting up any necessary trusts, reviewing beneficiaries, and making sure your healthcare directives and power of attorney are in order. It’s not about being morbid; it’s about making life easier for the people you care about.

Also, if you’re in your 60s and involved in crypto, it’s probably time to prioritize Bitcoin above all other cryptocurrencies. The volatility of assets beyond Bitcoin likely isn’t a good fit for your portfolio - unless you’ve explicitly accounted for that level of risk.

If you’ve missed any of the steps mentioned above, don’t panic - go back and tackle them! If you’re in your 60s but find yourself financially where many people are in their 40s, that’s okay. This doesn’t mean planning to live into your 100s; it means accelerating your timeline while staying focused on what needs to be done and continuing to plan for your future. Your timeline might be a bit off, but it’s never too late to get on track and build a secure financial foundation.

If everything goes perfectly according to plan, you may get to witness the eighth wonder of the world in action. One million dollars invested - without any additional contributions - growing at a 7% annual return, compounded yearly over 10 years, becomes nearly $2 million. Where else can you earn close to a million dollars in a decade, or about $100,000 a year, just by sitting back and doing nothing?

Nowhere.

That’s all for today - I hope you enjoyed it. Now go enjoy life, and try not to overthink your net worth.

“Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn't, pays it.” Albert Einstein

Bitcoin Thoughts And Analysis

Today, I’m revisiting the Ichimoku Cloud system – a tool I used extensively in the past and still find incredibly useful for adding context to market structure. While I don’t use it as a primary system these days, it’s a fantastic way to gain a different perspective on price action, trend strength, and key support/resistance areas. The Ichimoku system, at its core, helps traders see the bigger picture at a glance by combining several indicators into a single, cohesive framework.

Looking at Bitcoin’s daily chart through this lens, we see that the price has lost the Tenkan-Sen as support. The Tenkan-Sen – or conversion line – acts as a dynamic gauge of short-term momentum, and losing it can be a warning sign that momentum is stalling. The next logical level to watch is the Kijun-Sen – or baseline – which sits in the 94,000–95,000 range. A test of this level would align with a potential period of consolidation or pullback unless Bitcoin can reclaim the Tenkan-Sen quickly.

It's also worth noting the Kumo twist – a shift in the color of the cloud from red to green – which signals a potential change in the longer-term trend bias. This is typically viewed as a bullish sign, especially when price is above the cloud itself. However, the Kumo twist alone isn’t a buy signal – it simply tells us the trend bias is starting to shift, and we still need price to hold above key support levels to confirm it.

Overall, while the cloud remains bullish with price above it and the Kumo twist suggesting a shift in sentiment, losing the Tenkan-Sen is a yellow flag. It’s not a full reversal signal, but it does suggest caution in the short term. If Bitcoin can hold above the Kijun-Sen and reclaim the Tenkan-Sen, the uptrend remains intact. But if we see a deeper move into the cloud, that could signal a more prolonged consolidation or even a correction.

This isn’t a forecast – just a reminder to stay balanced, challenge our own biases, and use different tools to see the market from multiple angles.

US Stock Futures Slip as Trade Uncertainty Remains

US stock futures declined as investors grapple with persistent trade tensions and a fog of uncertainty in global markets. S&P 500 futures dipped 0.5%, extending a choppy run of daily swings between gains and losses. Treasuries rose, bolstered by a strong demand for Japanese bonds, while the dollar firmed. The White House’s latest attempt to arrange a call between President Trump and Chinese President Xi Jinping has yet to find a receptive audience, fueling concerns about stalled trade negotiations with both China and the European Union.

The economic picture is clouded further by signs of softening in the US economy. The OECD warned that Trump’s trade policies have helped push the global economy into a downturn, with the US among the hardest hit. A report expected later today is forecast to show a drop in US job openings to the lowest level since 2020, while Friday’s payrolls data will likely reveal a slowdown in hiring. Market volatility remains elevated, and investors are struggling to find clarity, as highlighted by SGMC Capital’s Massimiliano Bondurri, who noted on Bloomberg TV that the back-and-forth in markets is a reflection of the need for greater visibility.

Across the Atlantic, European inflation cooled more than expected, dropping below the European Central Bank’s 2% target, fueling expectations for rate cuts. The Stoxx 600 trimmed losses, while the euro weakened 0.3% against the dollar. Traders are nearly certain the ECB will cut rates by 25 basis points on Thursday, with further reductions likely later in the year. Meanwhile, corporate headlines added to the uncertainty, with Toyota Industries receiving a $33 billion buyout offer, Thames Water’s rescue deal falling apart, and Taiwan Semiconductor Manufacturing Co. facing delays in Japan. These developments underscore the fragile state of markets, as investors navigate a complex web of geopolitical tensions, softening economic indicators, and corporate shakeups.

Stocks

The Stoxx Europe 600 fell 0.3% as of 10:09 a.m. London time

S&P 500 futures fell 0.5%

Nasdaq 100 futures fell 0.4%

Futures on the Dow Jones Industrial Average fell 0.4%

The MSCI Asia Pacific Index rose 0.2%

The MSCI Emerging Markets Index rose 0.4%

Currencies

The Bloomberg Dollar Spot Index rose 0.2%

The euro fell 0.3% to $1.1408

The Japanese yen was little changed at 142.84 per dollar

The offshore yuan rose 0.3% to 7.1882 per dollar

The British pound fell 0.2% to $1.3517

Cryptocurrencies

Bitcoin rose 0.2% to $105,185.28

Ether rose 2.6% to $2,606.9

Bonds

The yield on 10-year Treasuries declined three basis points to 4.41%

Germany’s 10-year yield declined three basis points to 2.50%

Britain’s 10-year yield declined six basis points to 4.60%

Commodities

Brent crude rose 0.2% to $64.79 a barrel

Spot gold fell 0.6% to $3,360.05 an ounce

Russia’s Largest Bank Launches Bonds Linked To Bitcoin

Sberbank has launched a new structured bond that ties investor returns to both the performance of Bitcoin and the USD-to-ruble exchange rate. This marks one of the first Bitcoin-linked investment products offered by a major Russian institution under newly updated regulations. The bond is initially available over the counter to a limited pool of qualified investors and does not require a Bitcoin wallet or use of foreign platforms - transactions are processed entirely in Rubles within Russia’s domestic financial system.

Sberbank also plans to launch similar Bitcoin-based investment products on the Moscow Exchange, including a Bitcoin futures offering via its SberInvestments platform, set to debut on June 4. These developments follow a recent policy change by the Bank of Russia that now permits financial institutions to offer Bitcoin-linked instruments to qualified investors. Russia has historically taken a cautious and restrictive stance toward digital assets, but following recent developments, that approach is beginning to shift.

Circle Is Set To Go Public Later This Week

Following BlackRock’s interest in purchasing 10% of Circle, the company is now aiming for a new valuation of up to $7.2 billion in its expanded U.S. IPO, which was previously set at around $6 billion. The firm and some of its investors also now plan to raise up to $896 million by offering 32 million shares at $27–$28 each, up from an earlier plan of 24 million shares at $24–$26.

For a long while, Circle has taken on some heavy scrutiny regarding its profitability metrics, but the company did register a 55% increase in reserve income last quarter and Circle’s transaction and distribution costs also surged, outpacing revenue growth. Also, this should bring a boost to Coinbase, a partner of Circle who distributes USDC and is one of the few other publicly traded crypto companies. Circle will trade on the NYSE under the ticker ‘CRCL,’ with J.P. Morgan, Citigroup, and Goldman Sachs leading the offering.

Consensys Closes Its Deal With SharpLink

I covered this story in detail last week, and now the deal is officially finalized. I believe this could mark a major development for Ethereum. If even one company can replicate what Strategy has done for ETH – even at a smaller scale – it could generate the positive sentiment Ethereum has been missing.

Based on conversations I’ve had within the industry, sentiment around ETH has improved significantly – but there’s still more work to be done. The trend is 100% moving in the right direction.

If you are an ETH investor, read the blog post the Foundation released yesterday:

“Over the last year, many of us concluded that we needed to do a better job articulating our priorities. In conversation with our community, our collective mind has produced three ambitious goals for us to achieve in short order: scale L1, scale blobs, improve UX. Doing so successfully is the most valuable work we could be doing on behalf of our community, and it is our responsibility to deliver on it.

It is time for us to ensure that these goals directly drive our attention and resource allocation. Each of these goals is now mapped to a strategic initiative for Protocol, a shared workspace to bring our complementary talents together. We encourage every team in Protocol to consider how their work is supporting our execution of these strategic initiatives.”

Also, SharpLink doesn’t seem to be stopping at $425m. Look at this:

If SharpLink pulls off a $1 billion ETH purchase, it would quickly become the largest publicly known holder of Ethereum - surpassing even Coinbase and the Ethereum Foundation.

Wall Street Panic As Bitcoin Holds Strong - Bottom Confirmed? | Macro Monday

Join Dave Weisberger, Mike McGlone, and James Lavish on this week’s Macro Monday as we break down the chaos in traditional markets. Stocks and treasuries are selling off hard — is this the signal that Bitcoin has finally bottomed? We dive into what’s really driving the market and where crypto fits into the storm. Don’t miss this one!

My Recommended Platforms And Tools

Aptos - The blockchain network with everything you need to build your big idea. Unrivaled Speed, Unprecedented Trust, and an Unstoppable Community on Aptos.

Arch Public - It’s a hedge fund in your pocket. Built for retail traders, designed to outperform Wall Street. Try emotionless algorithmic trading at Arch Public today.

Trading Alpha - Trade With Confidence! My new go-to indicator site and trading community. Use code '25OFF' for a 25% discount.

X - I spend most of my time on X, contributing to CryptoTownHall every weekday morning, sharing random charts, and responding to as many of you as I can.

YouTube - Home of the Wolf Of All Streets Podcast and daily livestreams. Market updates, charts, and analysis! Sit down, strap in, and get ready—we’re going deep

The views and opinions expressed here are solely my own and should in no way be interpreted as financial advice. Every investment and trading move involves risk. You should conduct your own research when making a decision. I am not a financial advisor. Nothing contained in this e-mail constitutes or shall be construed as an offering of financial instruments or as investment advice or recommendations of an investment strategy or whether or not to "Buy," "Sell," or "Hold" an investment.