The Most Cited Long-Term Concern About Bitcoin Just Got A Serious Institutional Answer

Fidelity Digital Assets published a two-part research series Tuesday taking the security budget concern seriously and answering it with the most complete institutional framework yet written.

There is a Bitcoin question that gets asked at every dinner I have with sophisticated investors, on roughly every panel I sit on, and in maybe half the DMs that hit my inbox in a given week. It goes something like this. Every four years the block reward halves. The subsidy paid to miners for securing the network drops by fifty percent. Eventually, the subsidy goes to zero. Transaction fees are supposed to replace it. What if they don’t? What if hash rate drops, attacks become economically viable, and Bitcoin’s security model breaks?

That is the security budget question. It is the single most cited long-term concern about Bitcoin in serious institutional discussions, and most attempts to answer it have been either dismissive or unconvincing.

Tuesday, Fidelity Digital Assets published a two-part research series taking the question seriously and answering it more completely than anything I have read this year. The series is good. It deserves to be engaged with.

Let me walk you through what Fidelity actually argues, what they get right, where the analysis could be more honest, and why this matters for how you should think about owning Bitcoin over the next two decades.

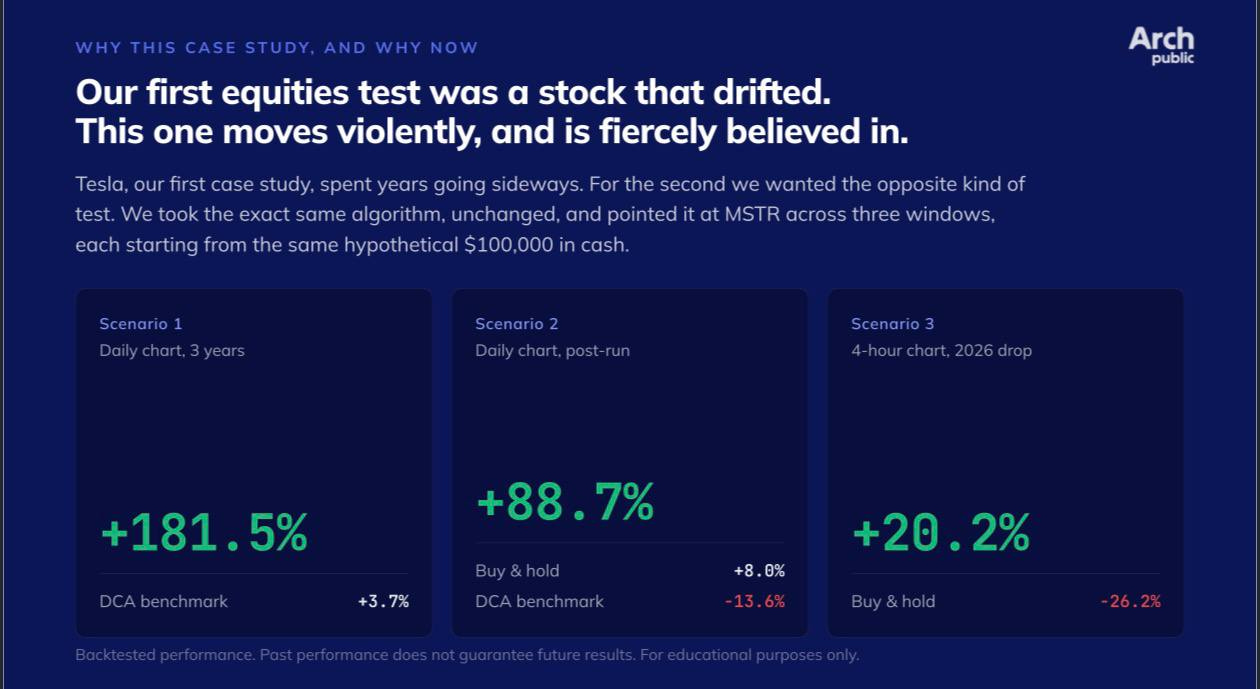

ARCH PUBLIC IS ADDING EQUITIES!

Arch Public is launching both equities and ETF agentic, algorithmic trading. Our tools are coming to the rest of your portfolio and we are starting with a bang!! Check out the numbers above on $MSTR. Incredible only begins to describe what our strategies accomplish with volatile assets.

Over the past three years if you aped in or DCA’d into MSTR our strategies crushed any and all returns. Even YTD returns are significantly positive.

Our strategies are coming to all the biggest names and ETF’s. Get in now - your portfolio deserves it!

Sign up for a demo HERE.

The Concern, Stated Honestly

Bitcoin’s monetary policy is rules-based, not opinion-based. Every four years, by design, the network cuts the block subsidy paid to miners in half. The first halving in 2012 took it from 50 bitcoin per block to 25. The second in 2016 took it to 12.5. The third in 2020 took it to 6.25. The fourth in April 2024 took it to 3.125. The fifth in April 2028 will take it to 1.5625. By 2040, the subsidy will be around 0.195 bitcoin per block. By the year 2140, the subsidy will be zero.

That schedule was Satoshi’s design choice and it is one of the things that makes Bitcoin Bitcoin. Fixed supply. Predictable issuance. No discretion. But it creates a forward-looking question that serious investors actually wrestle with. Hash rate, the computational power that secures the network, is incentivized by the dollar value of the rewards miners receive. The subsidy is half of those rewards. Transaction fees are the other half. As the subsidy declines, fees have to make up the difference, or hash rate falls, or both. If hash rate falls enough, the cost of acquiring fifty-one percent of it drops. If that cost drops below the value an attacker could extract by attacking the network, the model breaks.

That is the structural concern. It is not unreasonable. The bear case treats it as Bitcoin’s eventual undoing. Most institutional research treats it as something to be hand-waved past. Fidelity just published the first piece I have read that takes it as seriously as the question deserves.

Part One: The Price-Appreciation Argument

The first major argument is straightforward. The security budget concern has not actually been a problem so far because price appreciation has more than offset the declining subsidy.

Over Bitcoin’s life, the bitcoin-denominated subsidy has declined by ninety-four percent. Over that same period, the USD-denominated revenue going to miners has increased by approximately one hundred fifty-seven thousand percent. Even as the network has paid out fewer coins per block, those coins have appreciated enough that the dollar value flowing to miners has gone up by orders of magnitude. The network currently operates at roughly one zettahash per second. That hash rate is being voluntarily contributed by mining operations because the dollar economics still work.

The piece includes a forward-looking exercise estimating what price bitcoin would need to reach to sustain current miner economics through future halvings. It is a deliberately rough model, not a price prediction. But the directional point is well taken. Within reasonable assumptions about adoption and price, miner economics keep working through the next several halvings.

The honest caveat, which the piece acknowledges, is that this argument is structurally dependent on bitcoin continuing to appreciate. If it does, the math holds. If it does not, the math gets harder. The piece does not pretend otherwise. But it makes the point that the security budget concern has, so far, been wrong in practice. The model has worked for sixteen years. That is not a guarantee. It is a track record.

What Fifty-One Percent Actually Buys You

Part one also walks through what fifty-one percent control of hash rate actually gives an attacker, and what it does not. This is the section I want every serious bitcoin holder to read because it corrects misconceptions I see repeated constantly.

A double-spend attack lets an attacker rewrite recent transaction history by producing a longer chain than the network’s honest chain. To execute it, the attacker needs majority hash rate, and the deeper they want to rewrite, the harder it gets. Satoshi addressed this in the original whitepaper using the Gambler’s Ruin formula. The math is unforgiving. With majority hash rate, you can rewrite shallow blocks. The deeper you try to go, the more energy you have to spend producing competing blocks faster than the rest of the network. Six confirmations, the standard most exchanges require for settlement, makes the attack effectively impossible.

A censorship attack lets an attacker exclude specific transactions from the blocks they produce. To work as a sustained attack, the attacker needs not just fifty-one percent but closer to ninety-nine percent of hash rate, because anything below that means honest blocks find their way into the chain and excluded transactions get included by competing miners. Below ninety-nine percent control, the censorship attack defeats itself within six blocks.

Fifty-one percent control also does not give an attacker authority over Bitcoin’s ruleset. The twenty-one million cap stays in place. The block reward schedule stays in place. The consensus rules stay in place. An attacker with majority hash rate can disrupt transaction finality and impose censorship over short windows. They cannot change what Bitcoin is.

Fidelity uses a recent real-world example to make the point. On March 23 of this year, the Foundry USA mining pool produced seven consecutive blocks, briefly creating a two-block chain reorganization that orphaned valid blocks from AntPool and ViaBTC. The episode was not an attack. It was statistical variance, the kind of thing that happens occasionally when one pool controls roughly a third of network hash rate. The longest chain won. The orphaned blocks’ transactions went back to the mempool and got included in subsequent blocks. The system worked exactly as designed.

Part Two: The Difficulty Adjustment Is The Underrated Security Mechanism

This is the more sophisticated argument and the one I think most security budget discussions miss entirely.

Bitcoin has a built-in mechanism called the difficulty adjustment. Roughly every two weeks, the network recalibrates how hard it is to produce a valid block, targeting an average block time of ten minutes. When hash rate rises and blocks get produced too quickly, difficulty goes up. When hash rate falls and blocks get produced too slowly, difficulty goes down. The adjustment is algorithmic, not discretionary. It happens automatically. It has been happening every two weeks since 2009.

The central insight in part two is that the difficulty adjustment is the underrated piece of Bitcoin’s security model. Most analyses focus on absolute hash rate as the measure of security. The actual measure of security is the cost of attacking the network relative to the cost of honest participation. The difficulty adjustment continuously recalibrates that ratio.

Here is the logic. Suppose bitcoin’s price falls and hash rate drops by half as miners turn off unprofitable rigs. In absolute terms, the network is less secure. But the difficulty adjustment also drops by roughly the same amount. The cost of acquiring fifty-one percent of the now-smaller hash rate is lower, but so is the cost of mining honestly. The ratio between attack cost and honest participation cost stays roughly the same. The economic incentive to attack rather than mine honestly does not improve.

Fidelity runs through four scenarios. In the early years before 2010, hash rate was low and attacks were technically feasible, but bitcoin had no value worth attacking. In the growth years from 2010 to 2019, hash rate scaled with price, and the cost of attack stayed ahead of the cost of honest mining. In the current consolidation phase, hash rate has concentrated among efficient operators, but the difficulty adjustment maintains competitive balance among them. In a hypothetical future where bitcoin’s price stalls, hash rate may stagnate but the difficulty adjustment keeps the attack cost above the honest mining cost.

The conclusion is that the difficulty adjustment is the mechanism that preserves Bitcoin’s security across vastly different market conditions. Not the absolute level of hash rate. Not the absolute size of the security budget. The relative cost of attacking versus participating, recalibrated automatically every two weeks for the next hundred and fifteen years.

The Concrete Data Point That Proves The Fee Market Thesis

The most useful single piece of evidence in the entire series is the data from block 840,000, the block in which the fourth halving occurred in April 2024.

Block 840,000 generated approximately 37.626 bitcoin in transaction fees. The block subsidy that day was 3.125 bitcoin. The fees were roughly twelve times the subsidy. Total dollar value of fees in a single block was approximately 2.4 million dollars.

The spike was driven by traders competing to inscribe content on the halving block for symbolic reasons. Demand for block space spiked. Fees auctioned upward in real time as users repriced their transactions to ensure inclusion. The auction lasted roughly four minutes before the block was mined. If it had lasted the full ten-minute average block time, fees would have gone substantially higher.

Fidelity uses this example to make a structural point about how fee markets actually behave under stress. The same dynamic that produced 2.4 million dollars in fees at block 840,000 is the dynamic that would produce escalating fees during any sustained censorship attack. Users excluded from blocks reprice their transactions. The fee auction escalates. The economic incentive for honest miners to claim those fees grows. Hash rate moves toward where the rewards are.

That is not theory. It happened. The fee market response to demand pressure has already been demonstrated in real conditions. The argument that fees can rise to defend the network is no longer purely hypothetical.

Where The Analysis Could Be More Honest

The series is genuinely good. It is also a piece of research published by an institution that benefits from Bitcoin being a successful asset class. That does not invalidate the analysis. But it does mean a reader should engage critically rather than just nod along.

Two points deserve more scrutiny than the series gives them.

First, the price-appreciation argument requires bitcoin to keep appreciating at a reasonable rate. The piece acknowledges this in passing, but the structural dependency deserves more weight. If bitcoin’s exchange rate compounds at meaningfully slower rates than it has historically, the math gets harder. The model has worked for sixteen years. The next sixteen years are unknown, and the next hundred years are deeply unknown.

Second, the difficulty adjustment argument is mathematically sound but it has a quiet assumption embedded in it. The argument is that the cost of attacking relative to the cost of mining honestly stays balanced through the difficulty adjustment. That is true if mining honestly remains broadly profitable. If at some point mining becomes broadly unprofitable and hash rate collapses to a level where the absolute cost of attack becomes trivial in dollar terms, the relative argument has less practical force. The piece acknowledges this by noting that the persistence-of-demand assumption matters. But the question of how much demand is enough is not really addressed.

These are not fatal critiques. They are honest qualifications any sophisticated reader should hold alongside Fidelity’s argument. The series is strong. It is not the final word.

Why This Matters Now

We are entering the years when the security budget question actually gets tested at scale. The April 2024 halving cut the subsidy to 3.125 bitcoin. The April 2028 halving will cut it to 1.5625. The 2032 halving will take it to 0.78125. By 2040, the subsidy will be around 0.195 bitcoin per block, less than a tenth of where it sits today. The transition from subsidy-dominated miner revenue to fee-dominated miner revenue will play out over the next decade and a half.

Fidelity’s argument is that this transition is structurally fine because of the difficulty adjustment and the demonstrated capacity of the fee market to respond to demand pressure. Block 840,000 is the most compelling data point. The four-scenario analysis is the most complete framework I have seen written about this question.

The investors who actually engage with this material will think about Bitcoin’s long-term resilience differently than the investors who do not. The security budget question is not going away. It will get asked at every dinner I have for the next decade. What has changed is that there is now a serious institutional answer worth pointing people toward when they ask.

Fidelity just made the strongest institutional case to date that Bitcoin’s security budget concern is overblown. The argument is structurally sound. It engages with the strongest version of the bear case. It uses real data. It acknowledges its own assumptions. It walks through forward scenarios with appropriate humility about what it can and cannot predict.

It does not close the question entirely. Nothing can, because we are projecting decades forward and the actual answer depends on facts about adoption, demand, and price that nobody can know with certainty. But it raises the bar for how seriously the concern should be taken, and it provides a framework that holds up to scrutiny.

This is the kind of institutional research Bitcoin has needed. More of it, please.

I’ll see you tomorrow.

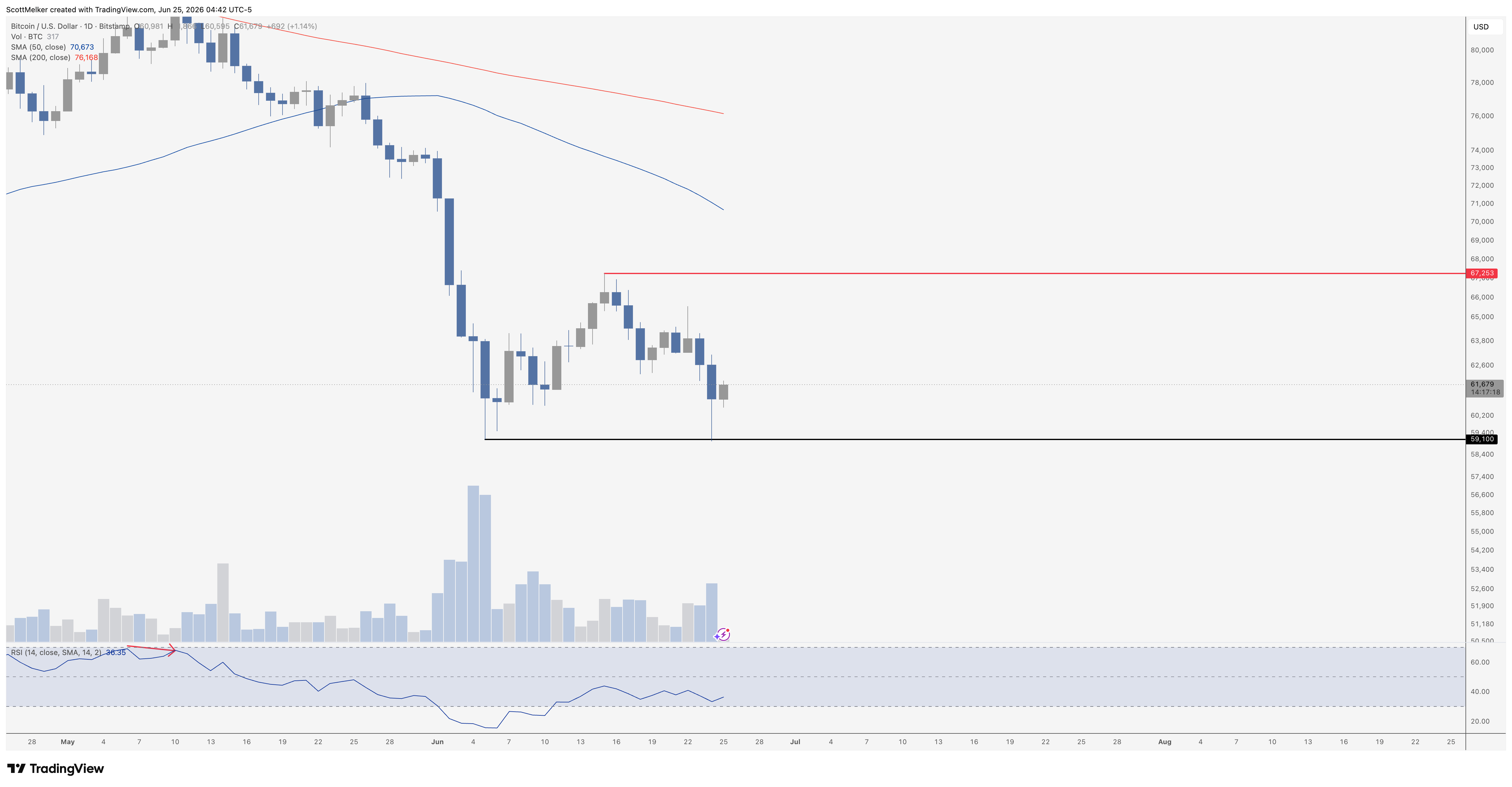

Bitcoin Thoughts And Analysis

As the critics write the Bitcoin obituaries for the 200th time, Bitcoin quietly sweeps the recent lows and forms a potential double bottom. A break above the $67,253 neckline would confirm.

Here are a few obituaries that I read this morning.

More importantly, the "it's over" posts came at the range lows, with nothing actually changing from a technical perspective. Classic panic at support.

Bitcoin is still sideways in June.

Binance Just Lost Its MiCA Application In Greece

Binance head of Europe says firm staying despite Greek MiCA setback

Binance’s bid to secure a passporting license through Greece has collapsed, head of Europe and UK Gillian Lynch told Reuters Tuesday. The exchange is now pursuing alternative regulatory pathways across the EU. Binance’s European fate has been the defining MiCA-era question for the largest exchange in crypto, and Greece was supposed to be the answer.

Chainlink Just Partnered With 47 Banks For Cross-Border Settlement

Chainlink teams up with 47 South Korean, European banks to speed up international money transfers

Chainlink announced Project Pangea Tuesday, an alliance with forty-seven South Korean and European banks aiming to use stablecoins to settle multimillion-dollar currency trades between the two regions in near real time. The project would compress settlement windows from days to minutes, replacing the correspondent-bank rails for a meaningful slice of EUR-KRW flow.

Hyperscale Data Just Took Its Bitcoin Treasury To 727 BTC

Hyperscale Data Bitcoin Treasury Reaches Approximately 727 Bitcoin

HPC infrastructure firm Hyperscale Data disclosed Tuesday that its bitcoin treasury holdings have reached approximately 727 BTC. The Nevada-based company has been quietly accumulating since 2024 as part of a treasury strategy explicitly modeled on the playbook Strategy made famous. The corporate treasury cohort continues to widen.

Bitcoin SHATTERED A $6B ETF Record – $10.6B Friday Expiry Hits

My Platforms And Sponsors

Arch Public - It’s a hedge fund in your pocket. Built for retail traders, designed to outperform Wall Street. Try emotionless algorithmic trading at Arch Public today.

Promote your brand with The Wolf of All Streets. For sponsorship and partnership opportunities, contact info@thewolfofallstreets.io.

The Wolf Pack - My Telegram group where I share daily market updates, real-time observations, and ongoing discussions with the community. There’s a dedicated channel and group chat, and it’s completely free to join.

The Crypto Advisor - My weekly newsletter for registered investment advisors, combining macro trends, Wall Street insights, and crypto – all in one place..

X - I spend most of my time on X, contributing to CryptoTownHall every weekday morning, sharing random charts, and responding to as many of you as I can.

YouTube - Home of the Wolf Of All Streets Podcast and daily livestreams. Market updates, charts, and analysis!

The views and opinions expressed here are solely my own and should in no way be interpreted as financial advice. Every investment and trading move involves risk. You should conduct your own research when making a decision. I am not a financial advisor. Nothing contained in this e-mail constitutes or shall be construed as an offering of financial instruments or as investment advice or recommendations of an investment strategy or whether or not to "Buy," "Sell," or "Hold" an investment.

Thanks for reading The Wolf Den! Subscribe for free to receive new posts and support my work.

Strong piece, and the difficulty adjustment section deserves the emphasis.

The point most coverage misses is that it holds the ratio of attack cost to honest mining cost steady through any swing, which is what lets the system degrade gracefully rather than break.

The one thing I would push on is the fee market, which is treated as more settled than it is. It helps to keep the whole dependency chain in view.

-Security comes from hash rate,

-Hash rate is funded by the dollar value of subsidy plus fees,

-The subsidy's coin amount shrinks on a fixed schedule so its dollar value rides entirely on price,

-Fees ride on blockspace demand, which is decoupled from price.

That last link is the crux. Fees pay for bytes, not for value moved, so a very valuable but lightly used chain produces a thin fee market.

The clean anchor is the break-even.

A halving needs roughly 19 percent annual appreciation just to hold the dollar subsidy flat.

Above that line, halvings are close to a non-event and the concern is a tail risk.

Below it, fees have to do real work, and whether a deep fee market emerges from high-value settlement is the one genuinely open variable.

What I am actually watching, in order:

-The fee-to-subsidy ratio holding a durable floor outside the mania spikes,

-Hash rate and hashprice through the 2028 halving, and

-Base-layer demand from high-value settlement as everyday payments move to Lightning.

The real test runs across the next three halvings, not at 2140.

A valuable reminder that the biggest risks are often the ones that compound quietly over time.