The Bitcoin Product Stack Just Matured In Eight Weeks

BlackRock, Goldman, Franklin Templeton, and Coinbase all moved on structurally new Bitcoin products inside the same eight weeks while almost nobody named the pattern

For most of bitcoin’s history, owning it was simple. You bought some, you held it however you held it, and you waited for the next cycle. That was the product. Sophisticated wrappers existed for the institutions, sure, but for the investor sitting at home thinking about their portfolio, the question was always binary. Do you own any of it or do you not. The wrappers around the question kept changing. The question itself did not.

That ended over the past eight weeks. I am not sure most readers have processed what just happened.

Let me lay out what is actually in the market or about to be in the market, because I think the synthesis is more important than any single launch.

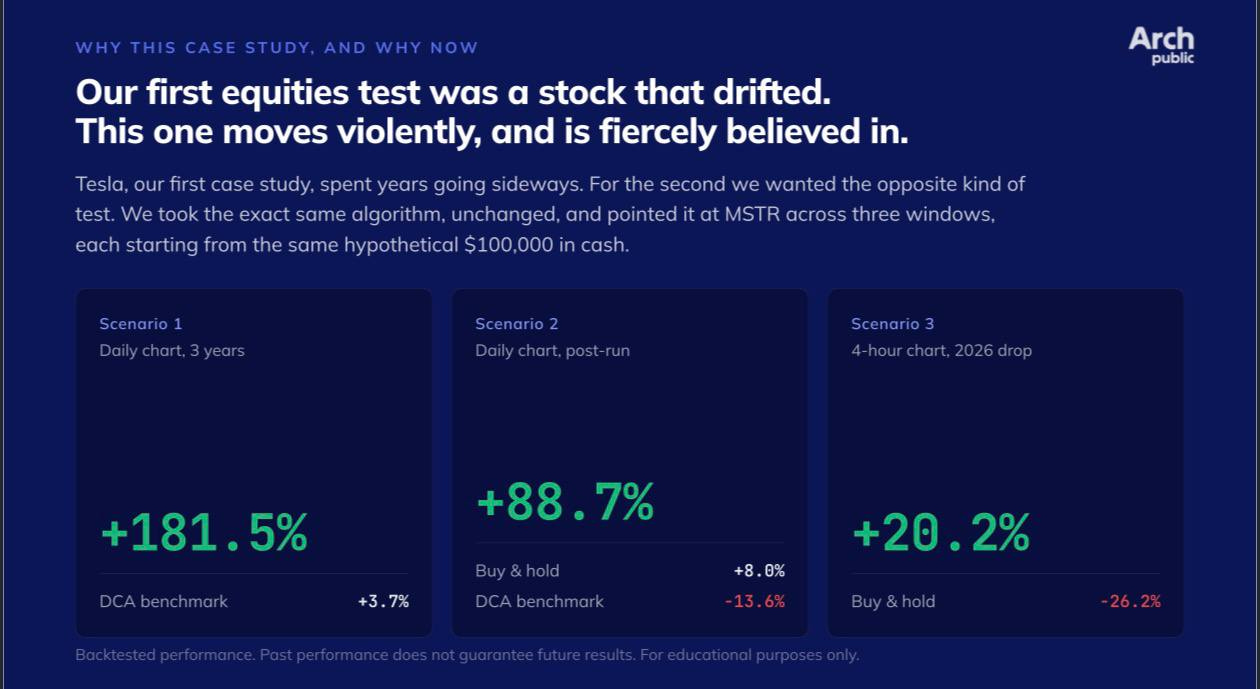

ARCH PUBLIC IS ADDING EQUITIES!

Arch Public is launching both equities and ETF agentic, algorithmic trading. Our tools are coming to the rest of your portfolio and we are starting with a bang!! Check out the numbers above on $MSTR. Incredible only begins to describe what our strategies accomplish with volatile assets.

Over the past three years if you aped in or DCA’d into MSTR our strategies crushed any and all returns. Even YTD returns are significantly positive.

Our strategies are coming to all the biggest names and ETF’s. Get in now - your portfolio deserves it!

Sign up for a demo HERE.

On June 16, last Tuesday, BlackRock listed the iShares Bitcoin Premium Income ETF on Nasdaq under the ticker BITA. The fund holds spot bitcoin and shares of BlackRock’s flagship IBIT spot Bitcoin ETF, and writes monthly covered call options on roughly twenty-five to thirty-five percent of its net asset value. The option premiums are distributed to investors as monthly income. The fund targets fifteen to twenty-five percent annual yield while retaining roughly seventy percent of bitcoin’s upside. The expense ratio is sixty-five basis points. BlackRock filed the final 8-A on June 11 and launched five days later, racing to get to market roughly two weeks ahead of Goldman Sachs, whose structurally similar Bitcoin Premium Income ETF was filed in April and is expected to become effective around July 1 under the standard SEC seventy-five-day registration clock.

Read those numbers again. The largest asset manager in the world, the issuer of the largest spot Bitcoin ETF on earth, just built and launched a structured income product directly on top of their own spot Bitcoin ETF. Two weeks later, Goldman Sachs is launching the same type of product. These are the two most consequential names in institutional asset management. They are not making sequential decisions about whether bitcoin is real. They are racing each other to the next product layer.

The same Tuesday that BlackRock launched BITA, Coinbase rolled out the largest product update in its history. The exchange now offers stock and ETF trading. Options on stocks and crypto. Pre-IPO perpetual futures on SpaceX, with OpenAI and Anthropic to follow. A registered AI advisor. A USDC credit card with five percent bitcoin rewards on travel spending. A user can now allocate a portfolio across stocks, ETFs, options, crypto, pre-IPO derivatives, and stablecoin payments without leaving the application.

Three days later, on Friday June 19, Franklin Templeton, a one-point-seven-trillion-dollar asset manager, filed two new ETFs with the SEC. The Franklin US Equity Bitcoin DRIP Index ETF and the Franklin US Innovation Bitcoin DRIP Index ETF would each hold a basket of large-cap US stocks weighted at roughly ninety-five percent of net asset value, with the remaining five percent in bitcoin exposure. Dividends from the underlying equity holdings would be systematically reinvested into bitcoin rather than back into the equity portfolio, with quarterly rebalancing trimming the bitcoin allocation back to four-and-a-half percent when reinvestment pushed it above five, and a hard twenty percent cap on bitcoin between rebalancing dates. Target effective date is September 1, 2026. This is a product category that did not exist a month ago. It is not a bitcoin ETF or a stock ETF. It is an equity income vehicle that automatically converts traditional corporate cash distributions into bitcoin exposure on a quarterly basis. The structure is a genuinely new wrapper, and one of the largest asset managers on earth is the one filing for it.

In the same eight-week window, Digital Credit, the asset class built around Strategy’s STRC and Strive’s SATA preferred stock complexes, just had its first major stress event. STRC traded as low as eighty-two dollars and fifty cents intraday last Thursday before recovering. SATA went from par down to the low nineties before bouncing equally hard. Matt Cole, the Strive CEO, published a thread on X explaining the dynamics as a leverage liquidation rather than a credit event, and the asset class largely survived its first real test. I wrote about it Friday. The point I want to make today is different. The fact that there is now an asset class called Digital Credit, with multiple issuers, billions of dollars of outstanding paper, and enough institutional participation to produce a real leverage cascade, is itself a maturation event. Eighteen months ago this asset class did not exist as a category. Today it is generating its own boom-bust cycles.

The Fed, Treasury, OCC, FDIC, FinCEN, and NCUA jointly proposed customer identification program rules for payment stablecoin issuers on the same Thursday, implementing the GENIUS Act. That is six federal agencies producing coordinated rulemaking around a payment-rail infrastructure that did not have any federal framework eighteen months ago. The rules are not the product. The product is the regulatory clarity that allows institutional capital to build products on top of the rails. The product, in other words, is the green light.

And underneath all of that, the stablecoin market itself continued its quiet build-out. Tether Gold options launched on Bybit. Ledn added Tether Gold to its lending platform. Drift Protocol continued its transition to USDT as its core settlement layer after the April exploit. The Hong Kong Monetary Authority’s stablecoin issuer guidelines went into effect. The plumbing kept building while everyone watched the price.

I want to step back from the inventory and make the structural argument, because the synthesis is the point.

Every mature asset class develops a predictable product stack over time. The arc looks roughly the same in every case. Spot exposure comes first. Then derivatives, including futures and then options. Then ETFs. Then leveraged and inverse ETFs. Then income overlays, including covered calls, defined-outcome funds, and structured notes. Then yield-bearing wrappers. Then automated allocation vehicles like target-date funds and DRIP products. Then synthetic exposure through baskets, indices, and tokenized wrappers. Each layer is built on top of the prior layers. Each layer expands the addressable investor base, because each layer matches a different investor’s specific need for yield, tax treatment, risk profile, or operational simplicity.

US equities took roughly a century to build that full stack. Gold took roughly fifty years from the launch of gold futures on COMEX at the end of 1974 to the current product complex. Bitcoin just compressed the same arc into roughly the last eighteen months, with the most consequential product layers built in the last eight weeks.

That compression is the story.

The reason it matters is that asset class maturation changes the question every investor faces. For most of bitcoin’s history, the question was binary. Do you own it or not. That was the question because spot ownership was the only meaningful way to express the view. The presence of a futures market or a single ETF did not really change the question. It just changed the wrapper. What has changed in the last eight weeks is that there are now genuinely different ways to express a bitcoin view that produce structurally different outcomes for different investor types. Income-oriented investors can buy BITA and capture fifteen to twenty-five percent yield from bitcoin’s implied volatility while still participating in roughly seventy percent of the upside. Tax-sensitive investors can hold IBIT in their taxable accounts and a bitcoin DRIP product in their retirement accounts to manage tax lots differently. Conservative investors who want bitcoin exposure but cannot stomach spot volatility can hold the equity-dividend wrappers that smooth their entry. Aggressive investors can lever Digital Credit preferreds for enhanced carry, and now have an idea of what happens when that leverage stack unwinds.

The question is no longer whether to own bitcoin. The question is which wrapper, in what size, for what tax treatment, with what yield overlay, in which account, with what counterparty risk profile, paired with what hedges. That is the same question sophisticated investors ask about US equity exposure. It is the same question sophisticated investors ask about gold exposure. It is the question sophisticated investors ask about every mature asset class, because every mature asset class offers enough different wrappers that the wrapper choice itself becomes the alpha.

I want to be honest about the complications, because this is not a victory lap.

The first is that product proliferation is not the same thing as product quality. The early years of any asset class involve products that look genius in good times and break in stress. Last Thursday’s Digital Credit leverage flush was the first real example in this cycle. There will be others. The covered-call income ETFs sound terrific in sideways markets and look meaningfully worse in sharp upside moves where the call options cap the upside on the hedged portion of the book. The equity-dividend wrappers are elegant in theory and untested in practice. Some of these products will not be in the market three years from now. Investors should treat the new wrappers with appropriate skepticism even as they treat the asset class with appropriate seriousness.

The second is that compression carries risk. The reason it took US equities a century to build a comparable product stack is that each layer was tested by multiple market cycles before the next layer was added. Bitcoin has not had that luxury. The product stack is being built in real time, with real capital, and many of the structural vulnerabilities will only be discovered the next time the market hits real stress. Friday’s leverage flush in Digital Credit is one early example. There will be more.

The third is that institutional product proliferation can change the underlying asset’s character. Bitcoin’s appeal for many of its long-time holders was specifically that it sat outside the traditional financial system. A bitcoin held in self-custody has no counterparty. A bitcoin held in BITA has BlackRock as the issuer, a regulated custodian holding the underlying assets, Nasdaq as the listing venue, and a network of options market makers writing the calls. That is not the same instrument. Both can be true at once. Bitcoin the protocol remains exactly what it has always been, while bitcoin the financialized exposure becomes increasingly indistinguishable from any other Wall Street product. The reader who internalizes this distinction has a clearer picture of what they are actually owning when they buy each wrapper.

The honest read is that bitcoin spent more than a decade being treated as a speculative instrument because the practical product stack to express the view differently did not yet exist. It is now an asset class. The investors who recognize that distinction position differently than the investors who do not. The investors who recognize it will think about wrapper selection, tax treatment, yield overlays, and counterparty risk the way they think about every other line item in their portfolio. The investors who do not recognize it will keep arguing about price.

The pattern is in the data. BlackRock launched the first major income wrapper last Tuesday. Goldman is two weeks behind. Franklin Templeton filed the first DRIP wrappers last Friday. Coinbase rebuilt itself as a multi-asset platform the same day BITA launched. Digital Credit survived its first stress test on the day before. The Fed, Treasury, OCC, FDIC, FinCEN, and NCUA produced coordinated stablecoin rulemaking inside the same week. The plumbing kept building.

This is what asset class maturation looks like from the inside. It rarely announces itself with a single headline. It accumulates as a series of individual launches that each look small in isolation and add up to something structural when viewed together. Eighteen months from now most of these products will be normalized portfolio components, and the conversations will be about the next layer.

For now, the data point worth holding onto is this. Eight weeks ago, the bitcoin product stack was thin enough that the question for most investors was still whether to own it. Today, the product stack is rich enough that the question is how. That is a meaningful change. It happened while you were watching the price.

I’ll see you tomorrow.

Capital B Just Got Approval To Raise €105 Billion For Bitcoin Purchases

Capital B shareholders approve €100B debt capacity to expand Bitcoin treasury

Europe’s first dedicated Bitcoin treasury company, Capital B, won shareholder approval Wednesday for up to €105 billion in financing capacity, including €5 billion in equity and €100 billion in credit instruments. The France-listed firm currently holds 3,139 BTC and targets 15,000 by 2027. Strategy’s corporate playbook just got formally adopted across the Atlantic.

The CFTC Just Permanently Banned Celsius Founder Alex Mashinsky

CFTC permanently bans Celsius founder Alex Mashinsky from U.S. commodity markets

The CFTC entered a consent order Thursday permanently banning Alex Mashinsky from trading or registering with the agency, closing its 2023 enforcement action over the Celsius collapse. Mashinsky is currently serving a 12-year prison sentence for fraud. The order resolves the regulator’s first enforcement case against a digital asset lending platform.

Microsoft Just Warned About Crypto Wallet Malware Spreading Via USB Sticks

Microsoft found malware that hijacks crypto wallets and spreads through USB sticks

Microsoft Threat Intelligence warned Thursday about new Windows malware that monitors clipboards to swap copied crypto wallet addresses for attacker-controlled ones, harvests seed phrases, and captures screenshots. The Trojan:Win32/CryptoBandits.A strain has infected endpoints since February and spreads via USB drives using Tor for command-and-control.

Bitcoin Just Hit Its $28 Trillion Tipping Point - Ex-CFTC Insider Caroline Pham

“I’m Buying Bitcoin Like Crazy” - Grant Cardone

My Platforms And Sponsors

Arch Public - It’s a hedge fund in your pocket. Built for retail traders, designed to outperform Wall Street. Try emotionless algorithmic trading at Arch Public today.

Promote your brand with The Wolf of All Streets. For sponsorship and partnership opportunities, contact info@thewolfofallstreets.io.

The Wolf Pack - My Telegram group where I share daily market updates, real-time observations, and ongoing discussions with the community. There’s a dedicated channel and group chat, and it’s completely free to join.

The Crypto Advisor - My weekly newsletter for registered investment advisors, combining macro trends, Wall Street insights, and crypto – all in one place..

X - I spend most of my time on X, contributing to CryptoTownHall every weekday morning, sharing random charts, and responding to as many of you as I can.

YouTube - Home of the Wolf Of All Streets Podcast and daily livestreams. Market updates, charts, and analysis!

The views and opinions expressed here are solely my own and should in no way be interpreted as financial advice. Every investment and trading move involves risk. You should conduct your own research when making a decision. I am not a financial advisor. Nothing contained in this e-mail constitutes or shall be construed as an offering of financial instruments or as investment advice or recommendations of an investment strategy or whether or not to "Buy," "Sell," or "Hold" an investment.

Thanks for reading The Wolf Den! Subscribe for free to receive new posts and support my work.